Tiger Research: DeFi is modular, no risk

DeFi is moving towards modularization, the battle for risk management in Morpho, Euler and Aave。

This is byTime ResearchWritten. As institutional investors enter the chain lending market, DeFi is moving away from a single shared pool structure towards a new structure of risk segregation and professionalization of the division of labour at the operational level。

Summary of highlights

- The Lehman crisis and the Kelp DAO events revealed the same type of structural deficiencies: the single shared pool structure magnifies the risk of a single asset and transforms it into a systemic crisis. Traditional finance responded by separating each functional layer of the financial system。

- DeFi ecosystems are moving in the same direction, that is, towards a modular architecture centred on risk isolation。

- AS RWA ASSETS BEGAN TO FLOW ALONG THE CHAIN, THE RATE OF CHANGE ACCELERATED。

- In modularization structures, the capability of the operational layer to manage the product in practice becomes a key variable。

1. Lessons from the Lehman crisis

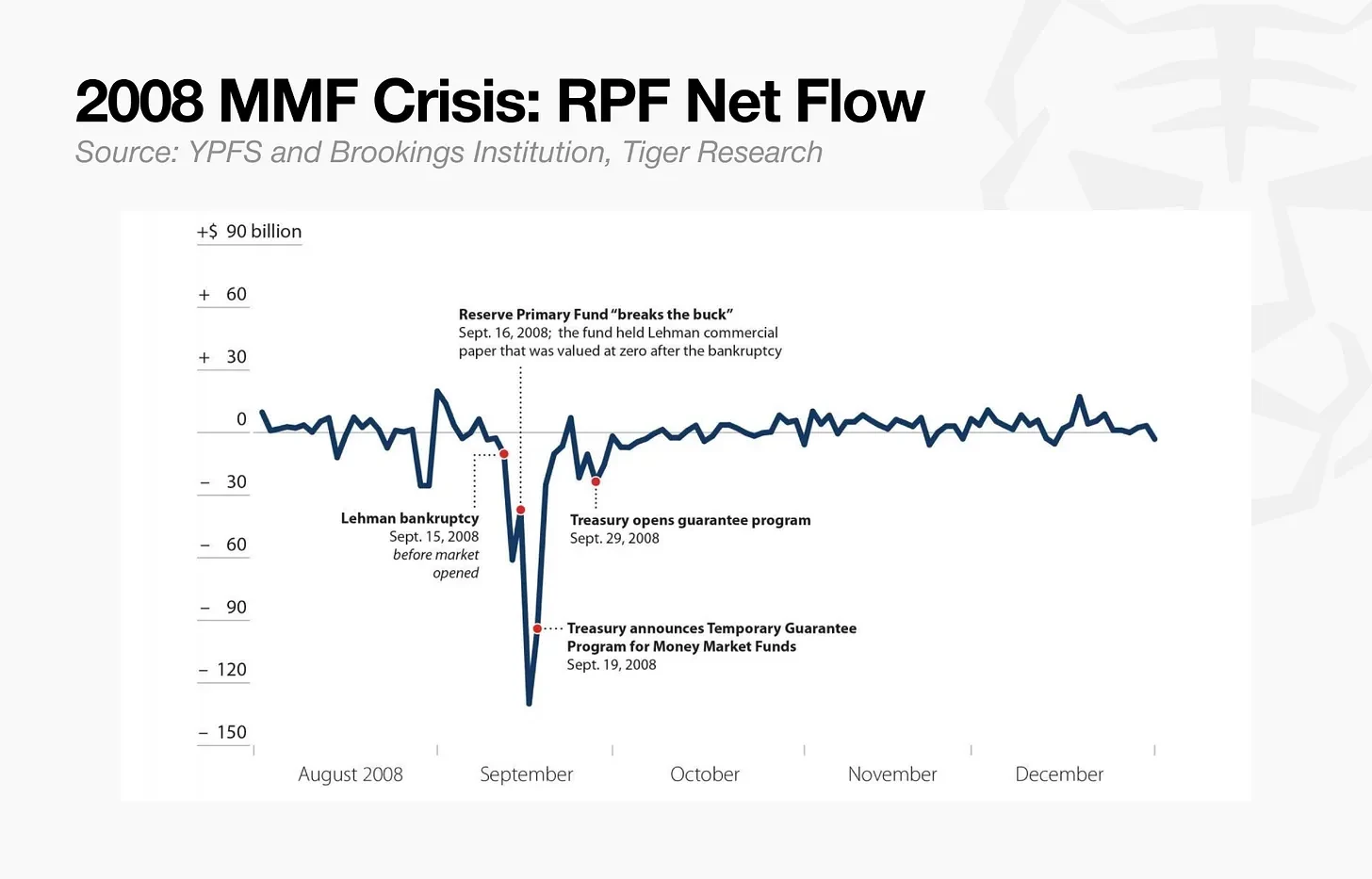

In September 2008, the collapse of Lehman Brothers triggered an unprecedented crisisTHE THIRD LARGEST GLOBAL MONEY MARKET FUND, THE RESERVE LEVEL FUND (RPF), SUSPENDED ALL FORECLOSURES WITHIN ONE DAY。

AT THAT TIME, RPF INVESTED ONLY 1.2 PER CENT OF ITS MANAGED ASSETS IN LEHMAN BROTHERS DEBT. AS A RESULT OF THE BANKRUPTCY OF THE LEHMAN BROTHERS, 1.2 PER CENT OF THE DEBT WAS UNCOLLECTIBLE AND THE TOTAL ASSET VALUE OF THE FUND FELL FROM 100 PER CENT TO 98.8 PER CENT OF NOMINAL VALUE. THIS IS SUFFICIENT TO BREAK THE BASIC PRINCIPLE OF MAINTAINING A FIXED NET ASSET VALUE OF $1 PER SHARE IN THE IMF INDUSTRY. THE VALUE OF EACH SHARE OF THE FUND FELL BY $1 TO $0.97。

The panic spread almost immediately after the loss of principal became apparent. The fear that waiting would lead to greater losses triggered an unprecedented run-off of banks, which in two days would be as high as $40 billion. Owing to such enormous pressure, the Fund frozen funds and stopped all withdrawals。

The collapse of the Lehman brothers forced a complete reorganization of traditional capital markets. In the area of monetary market funds, the guidelines on risk-graded liquidity buffers and foreclosure restrictions were thoroughly reformed. In the area of hedge funds, the industry has learned the lesson of Lehman Brothers re-mortgaging risk, i.e., a single-principal broker centralizing the customer ' s assets。

As a result, assets and credit are no longer concentrated in a single intermediary but have been restructured. The separation of the implementation infrastructure from risk management and the decentralization of risk exposure to multiple primary brokers have become criteria for global risk segregation。It is this institutional guarantee that separates infrastructure from risk in order to contain contagion that enables the asset management industry to rebuild operational trust and restore growth。

2. How traditional capital markets can address this problem

IN 2014, THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION RESTRUCTURED THE MONETARY MARKET FUND (MMF) FRAMEWORK. FUNDS ARE CLASSIFIED ACCORDING TO THEIR CAPITAL NATURE, AND DIFFERENT CRITERIA APPLY TO EACH FUND CATEGORY. THIS IS INTENDED TO PREVENT THE CROWDING OUT OR BANKRUPTCY OF ONE TYPE OF FUND FROM SPREADING TO OTHER TYPES OF FUND OR TO THE SYSTEM AS A WHOLE, EACH WITH ITS OWN BUFFER MECHANISM。

The core idea of traditional financial risk control methods is separation. Decentralization, avoiding the concentration of risk in a single chain, and introducing independent verification mechanisms at every stage of financial flows。

This principle is best reflected in the dominant brokerage in the capital market. Investment decision-making is in the hands of hedge funds, while risk regulation is exercised by brokers. The two functions are deliberately separated. In traditional lending markets, the same logic has been applied: credit assessment, underwriting, collateral management and trusteeship are the responsibility of separate independent bodies。

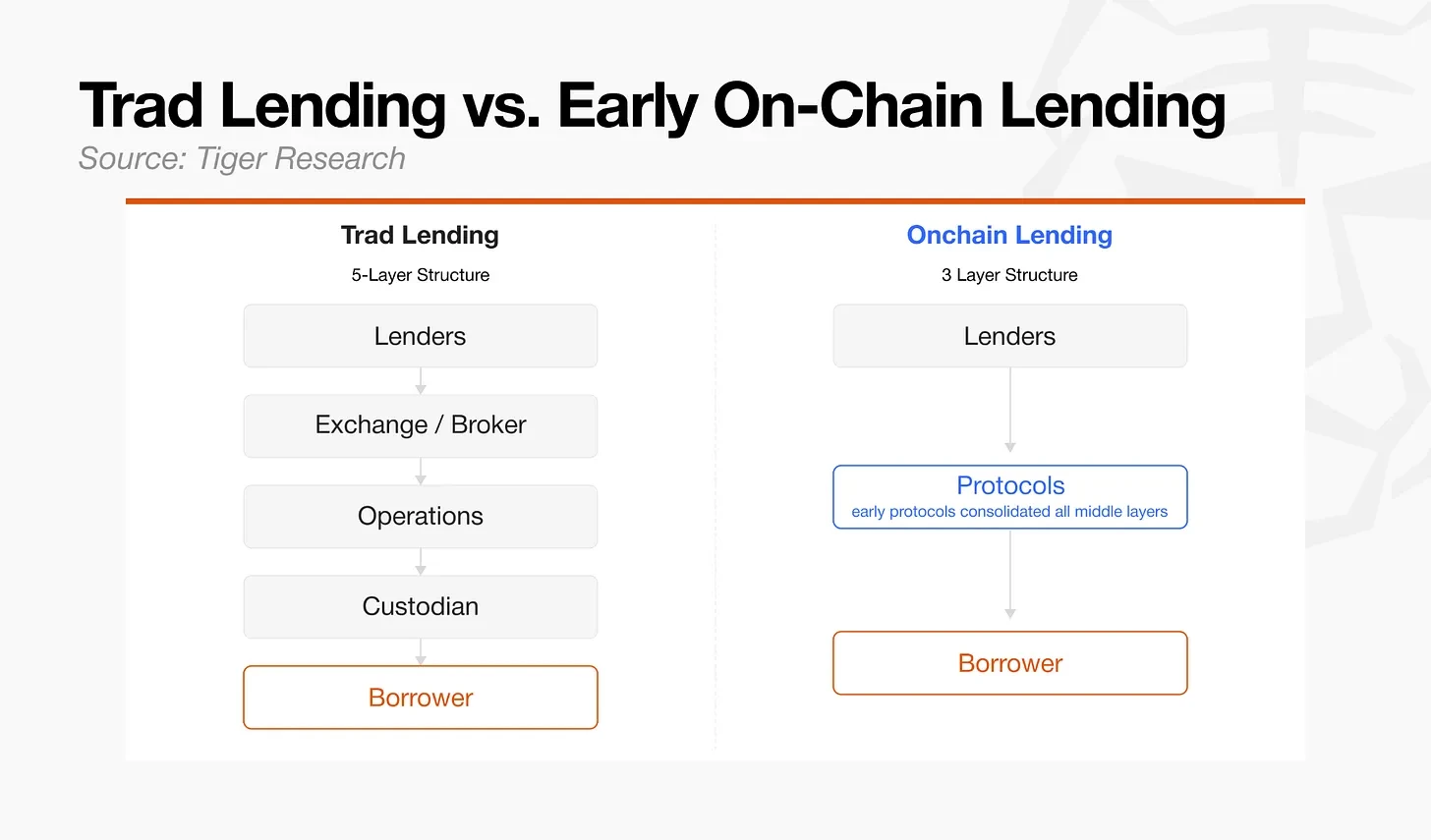

However, when asset management and lending began to migrate to DeFi, the multilayered intermediary structure of traditional finance was compressed into a single layer. The early DeFi agreement focused on removing the intermediaries needed to separate the structure, encode the mechanisms directly into smart contracts and automate processes previously handled by multiple participants。

3. From shared pool to modular structure

The early deFi approach of compressing all lending mechanisms into a smart contract reduced the costs of intermediaries, but also concentrated all risks in one agreement. Since credit evaluation, underwriting and collateral management all operate in the same code repository rather than as separate functions, defaults or failures in the liquidation of individual assets can directly paralyse the mobility of the system as a whole。

This potential risk of contagion forces the governing bodies of the agreement to set conservatively risk parameters. Assets with shorter or more volatile historical records, as well as any assets outside Bitcoin and the Ether House, are structurally excluded from collateral qualification. Compressing functions into individual contracts has led to a decline in capital efficiency: the diversification of assets is limited, as is market access。

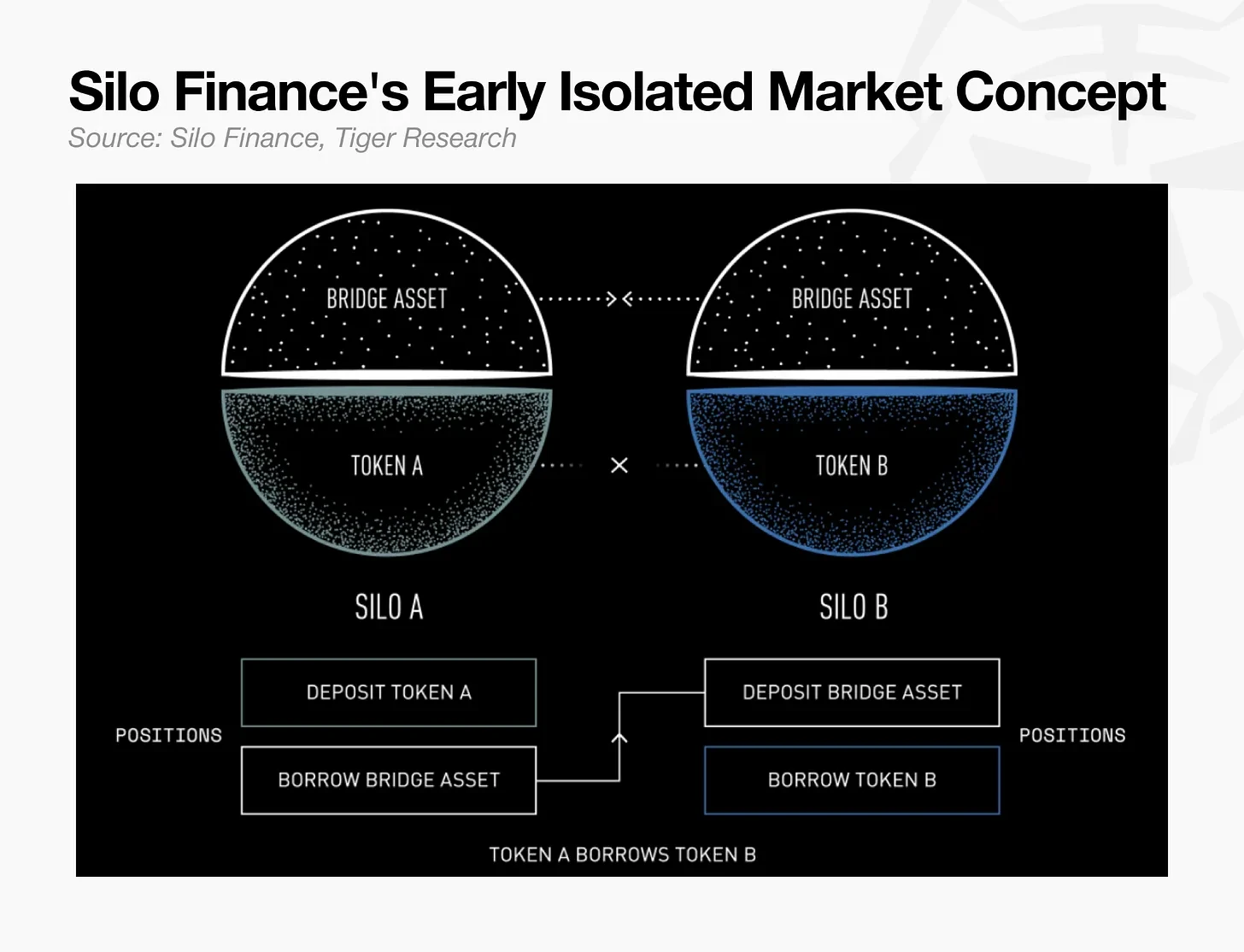

Silo Finance addressed the risk concentration of the unified asset pool by introducing a separate loan pool for each asset. By limiting price manipulation or the collapse of value to a single mortgage pool and preventing risk from spreading to other asset pools, Silo has proven that the threshold for governance approval can be lowered and new lending markets opened more quickly. The architecture shows that a single large asset pool can be divided and the risks segregated at the market level, while laying the foundation for subsequent modularization。

Silo ' s initial modularization system became the basic criterion for chain lending, as RWA assets, including monetized national debt and private loans, began to flow heavily into the chain. There are fundamental differences between each category of RWA in terms of transaction time, predictor reliability, regulatory requirements such as KYC and AML, and liquidation procedures. The early sharing pool model, which requires the use of a single unified set of parameters to manage such a diverse range of assets, is clearly not feasible。

THE INFLUX OF REAL WORLD ASSETS (RWA) HAS CREATED A NEED TO MOVE BEYOND SIMPLE ASSET SEGREGATION. IT REQUIRES THAT COMPLEX RISK CONTROL FRAMEWORKS IN TRADITIONAL FINANCE BE TRANSPOSED TO THE CHAIN ENVIRONMENT. AS ASSETS DIVERSIFY, THE CHAIN RISKS BECOME INCREASINGLY COMPLEX. TO CONTROL THESE RISKS, STRUCTURAL SEPARATION IS REQUIRED: ON THE ONE HAND, THE NON-REMOVABLE INFRASTRUCTURE LAYER RESPONSIBLE FOR LIQUIDATION AND SETTLEMENT, AND ON THE OTHER HAND, THE OPERATIONAL LAYER WITH REAL-TIME AUTHORITY TO ADJUST AND ASSUME RISK PARAMETERS。

The early decentralisation of finance (DeFi) was to compress the middle layer of finance into a single code bank. With the influx of RWA and the maturity of the lending market, the path to development has changed: liquidation and settlement efficiency have been entrusted to block chains, while the regulatory authority for risk has been separated to a separate level. In response to increasingly complex assets, chain lending has resulted in a structure similar to that of the traditional financial system (e.g., primary brokers and independent credit assessment), in which investment and risk monitoring have been separated. This modular structure has become the new standard for the chain lending market。

4. Institutional risk segregation and integration

Although the modularization architecture originated in the DeFi ecosystem itself, it coincided with the risk control standards required by institutional participants。

Morpho ' s decision to give priority to achieving complete risk segregation at the base structure level, even at the expense of a measure of capital efficiency, creates institutional needs. This demand has turned a turning point in the direction of other major loan agreements, especially those that initially adopted a shared pool structure。

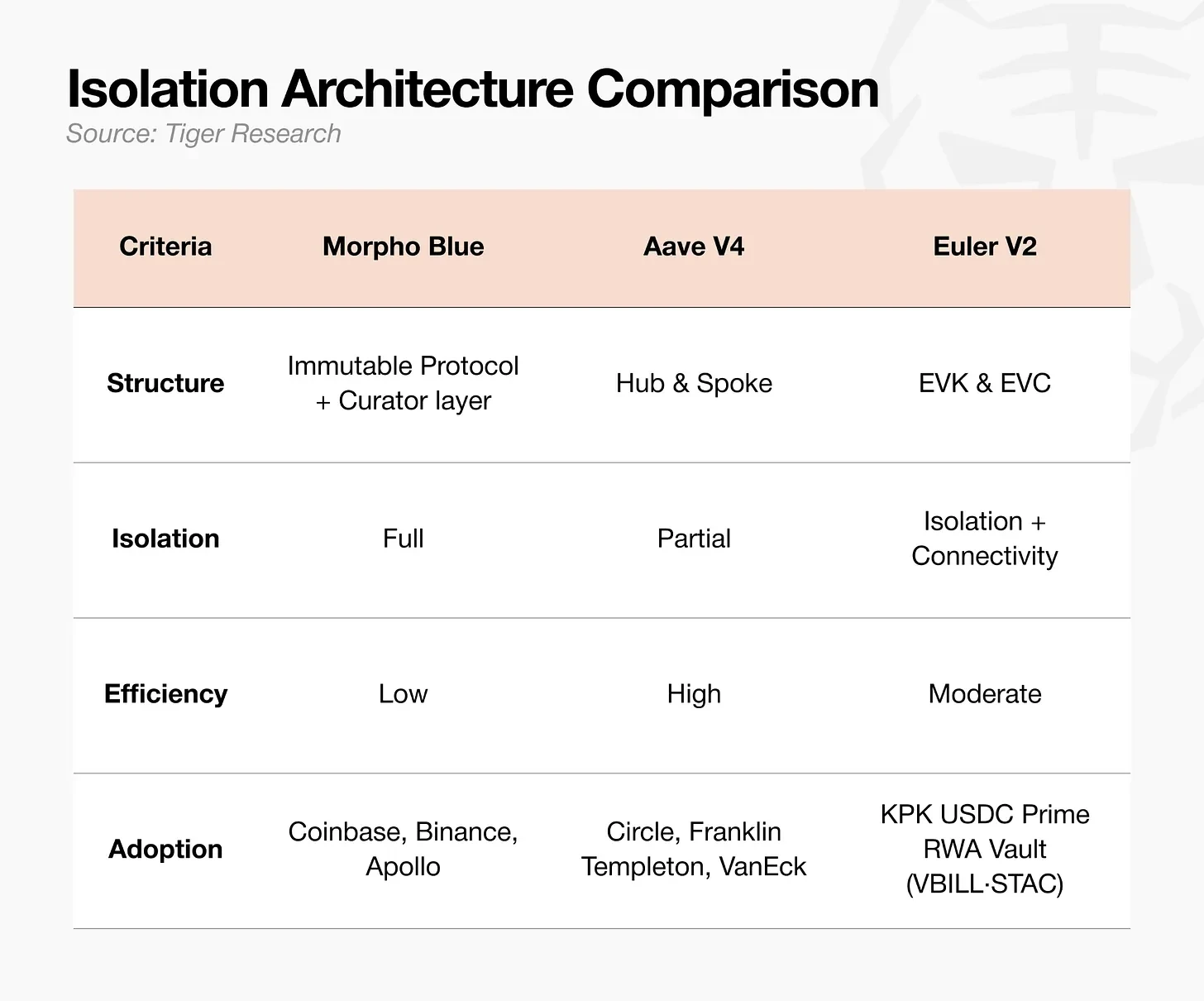

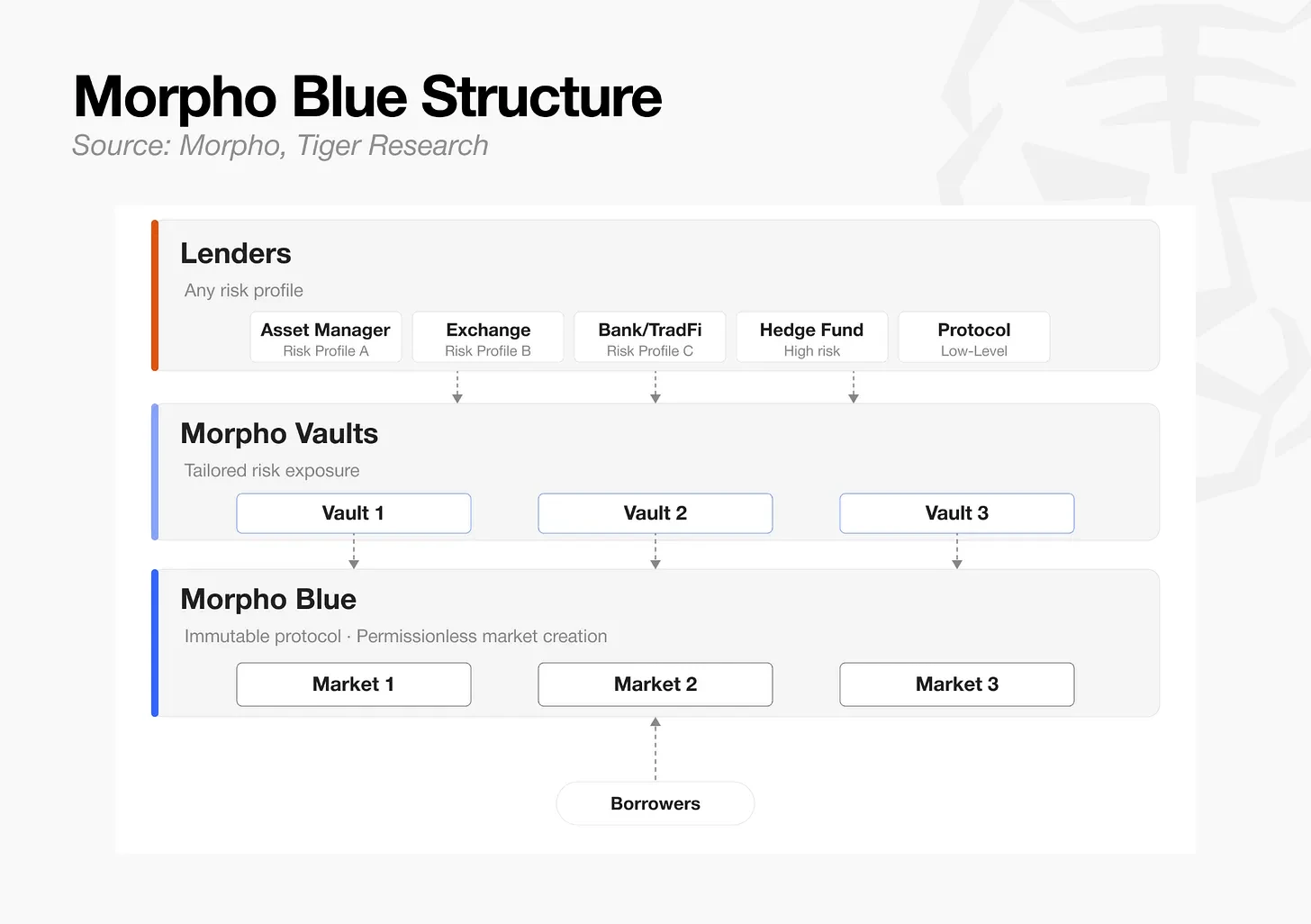

4.1 Morpho Blue: Main broker

Morpho was originally an intermediary level designed to optimize interest rates over first-generation DeFi lending agreements such as Aave and Compund. In this model, it cannot exist independently. In 2023, Morpho published the Morpho Blue White Paper and launched Morpho Blue and Morpho Vaults in early 2024, officially declaring their independent operation。

This shift abandons the structures that used to hold governance institutions hostage to all market risk decisions and separates market creation and risk judgement from the agreement itself. This separation forms the structural basis for institutional participants to select and control risks in accordance with their own standards of compliance。

Structure

- Morpho Blue: AN AGREEMENT THAT CANNOT BE ALTERED. AT THE TIME THE MARKET WAS CREATED, FIVE PARAMETERS WERE FIXED: MORTGAGED ASSETS, BORROWED ASSETS, LIQUIDATION LOAN VALUE RATIO (LLVV), PRICE INFORMATION AND INTEREST RATE MODEL. NO ONE CAN CREATE A MARKET WITHOUT A PERMIT. THE AGREEMENT ITSELF IS ONLY RESPONSIBLE FOR IMPLEMENTING PRE-WRITTEN CODES。

- Morpho Vaults• A risk management with an independent agent to select a qualified market, set supply limits and allocate funds. Each vault has a unique risk profile。

- LoaneeDEPOSITORS WITH VARYING RISK TOLERANCES, INCLUDING DAOS, PROTOCOLS, INDIVIDUALS AND HEDGE FUNDS, SELECT AND PROVIDE FUNDS THAT ARE APPROPRIATE TO THEIR CIRCUMSTANCES。

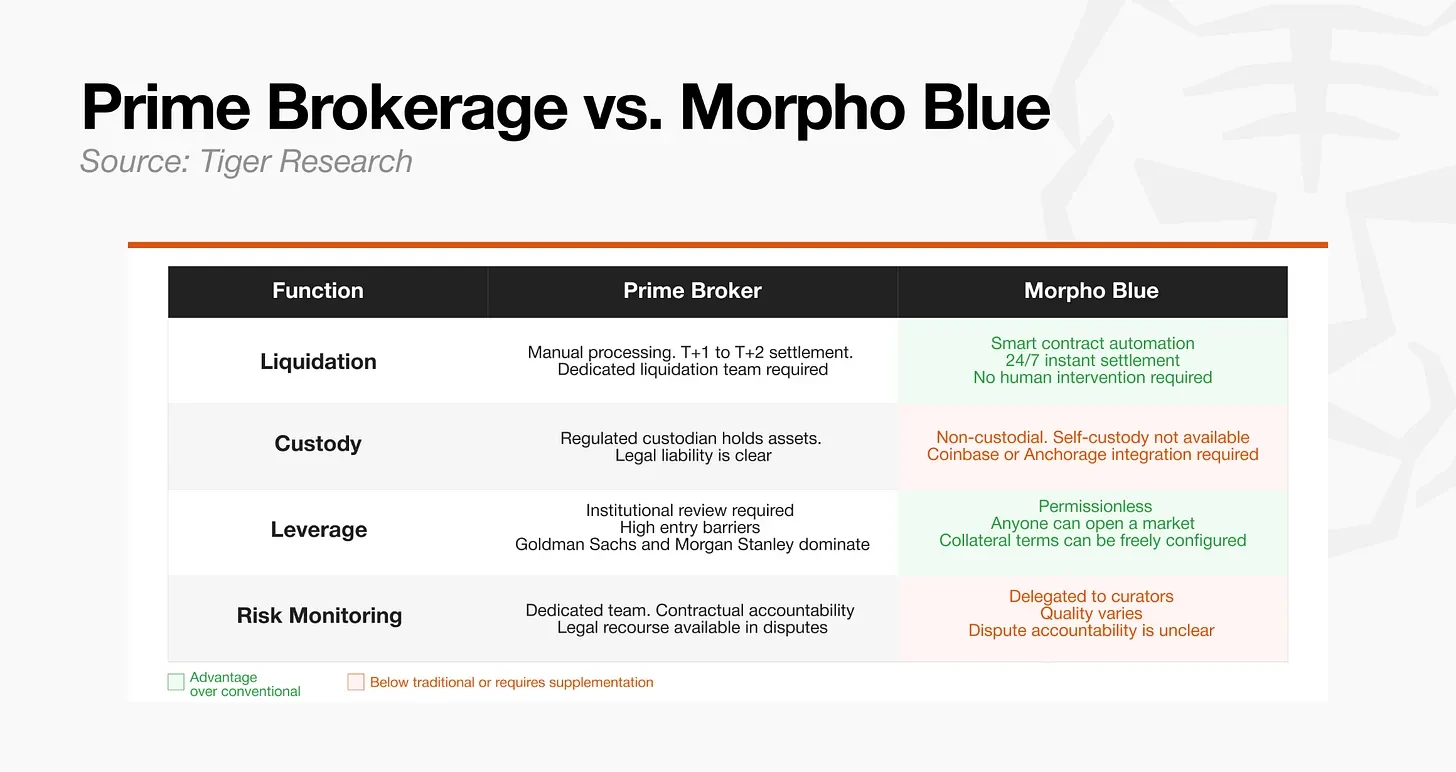

Traditional brokers are usually required to perform four functions: liquidation, trusteeship, leverage provision and risk monitoring. Morpho automating liquidation and leverage provision at the protocol level through smart contracts. However, because of its non-custodial structure, it is unable to provide the hosting environment required by institutional investors to meet regulatory requirements. Therefore, integration with external custodians such as Coinbase or Anchorage is necessary。

Similarly, risk control does not depend on the agreement itself, but on the ability of each custodian to select assets and manage risk exposures. This creates a continuing risk that the quality of the custodianship is uneven. This vulnerability was directly exposed by the events of 2025, XUSD and Stream Finance. Multiple Morpho vaults hold xUSD open and produce bad debts. Following the incident, the market began to examine more rigorously the asset selection and real-time risk management capabilities of the custodians, and corporate capital was concentrated on top-performing custodians such as Steakhouse, Gautlet and Setora。

Traditional brokering integrates liquidation, trusteeship, leverage and collateral management into one institution. Morpho replaced this model with a division of labour model, which assigns functions to professional participants within ecosystems rather than concentrating in one institution。

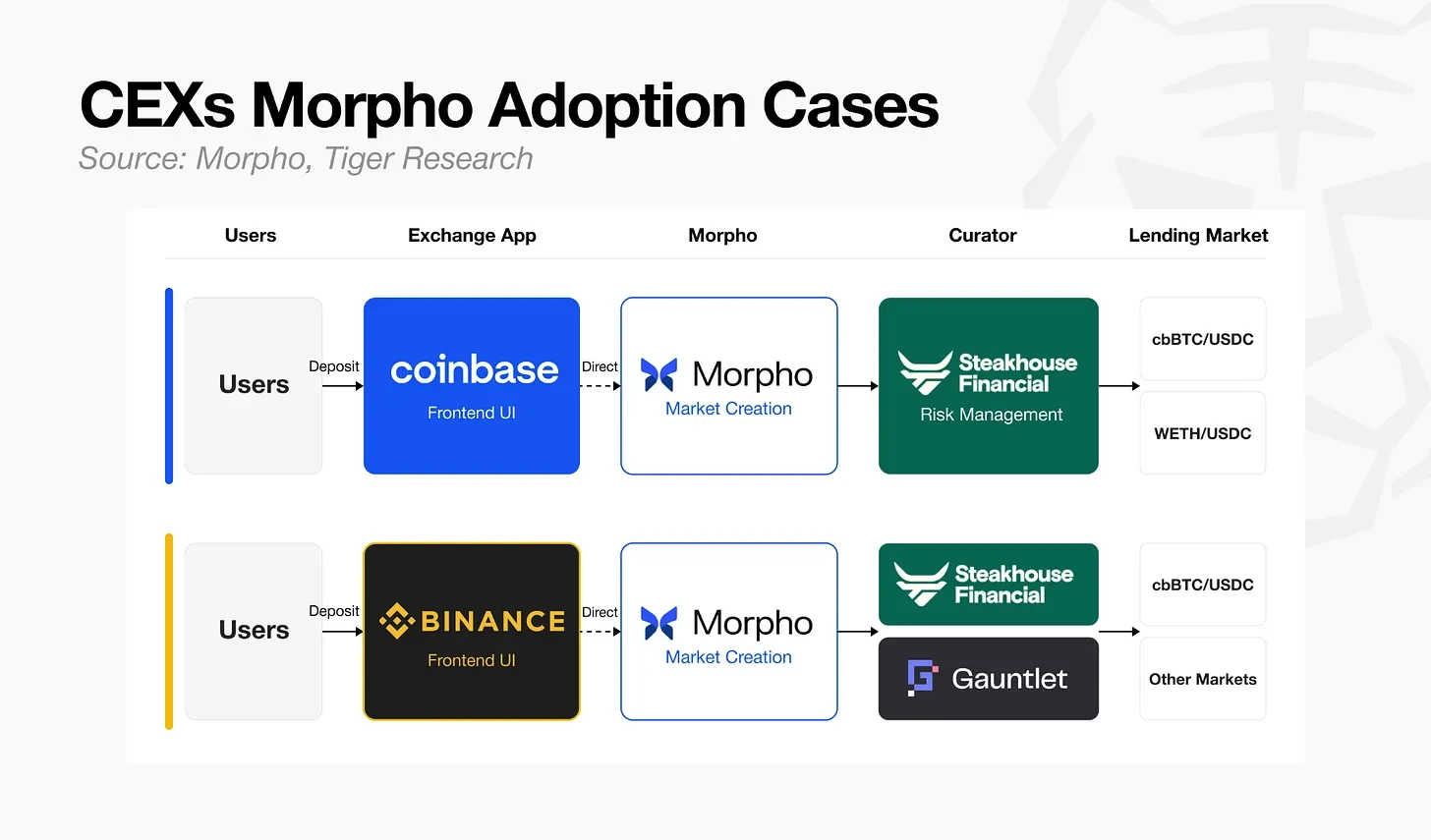

The introduction of institutions is taking place on a large scale, starting with a centralized exchange。

- CoinbaseUSDC lending service based on Morpho Blue, hosted by Steakhouse Financial。

- Currency: The same structure was adopted, with Steakhouse Financial and Gantlet acting as resource persons。

Users can obtain loans by clicking on the " Lending " button in Coinbase or currency-fix applications. The two exchanges with the largest global turnover chose the same structure. This structure has also been extended to traditional financial institutions。

- SG-FORGE& nbsp;: Deployment of stabilization currency EURCV and USDCV on the Morpho。

- ApolloThe private credit fund ACRED is chained and used as collateral for Morpho。

- Bitwise: Risk management directly above Morpho Vaults。

If monetization opens access to assets, Morpho opens the way for these assets to be converted into productive capital. The development trajectory set by Morpho is gradually showing a new direction of evolution, which is difficult to ignore for borrowing agreements with very different starting points。

4.2 Aave V4: General Bank

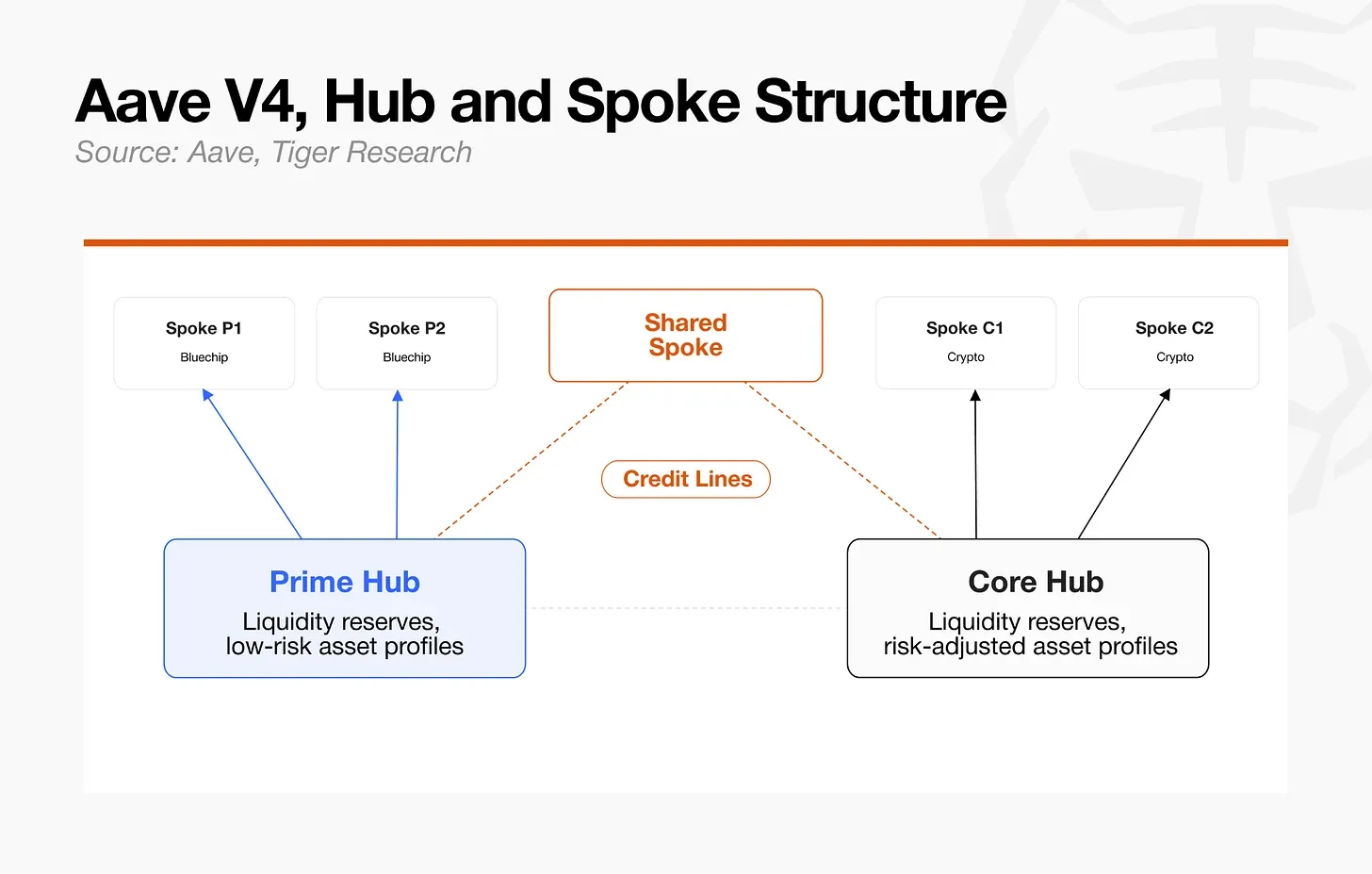

The original name of Aave, ETHLend, was a point-to-point loan matching platform, followed by three versions of V1, V2 and V3 and gradually developed into a shared pool structure. In March 2026, Aave launched a version of V4 on the Internet of the Improver, a modular structure. Unlike Morpho, which chose the structural separation of infrastructure from operations, Aave V4 chose a hybrid model to manage risk while maintaining liquidity efficiency。

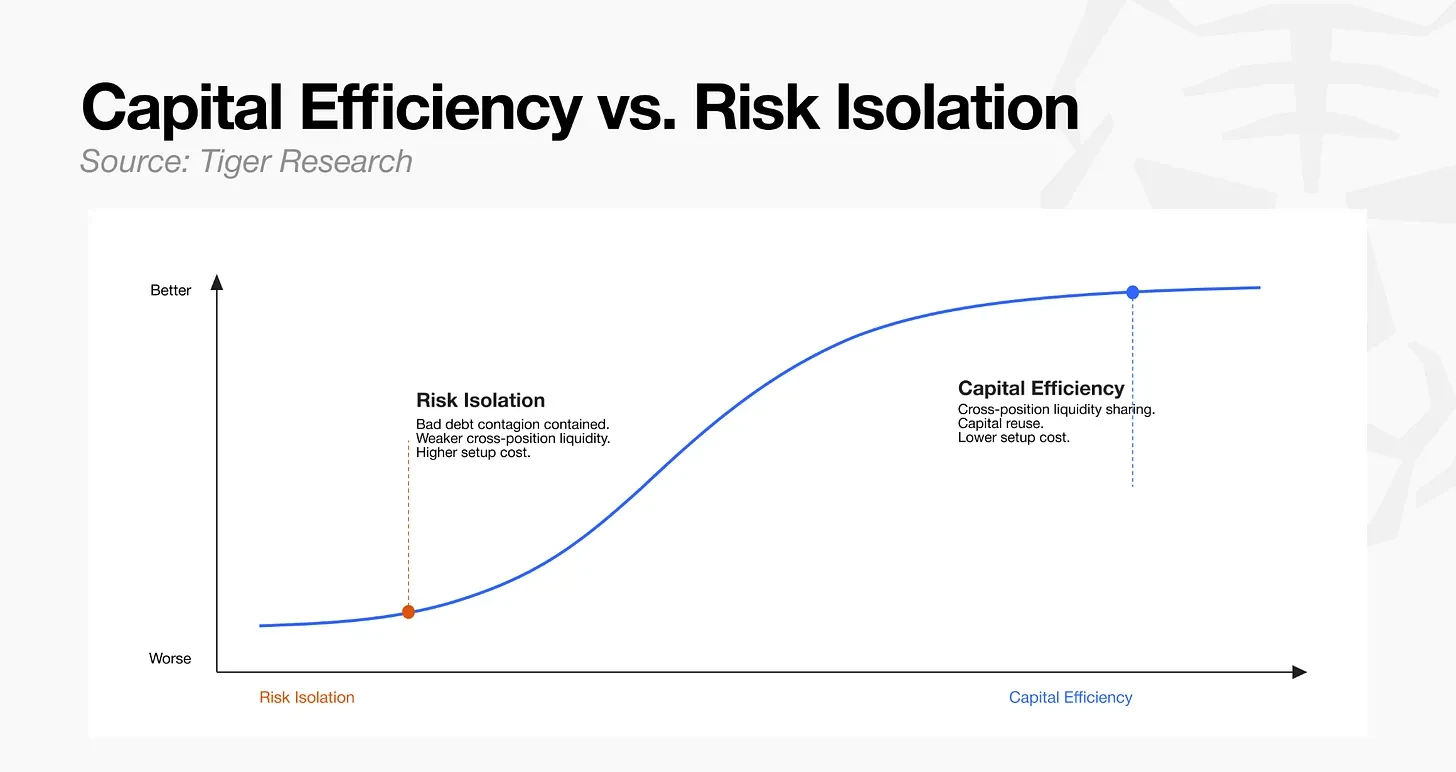

Aave is aware of the contradiction between risk segregation and capital efficiency. A move towards risk segregation could contain the spread of bad debt, but could weaken the liquidity network and reduce capital efficiency. V4 is designed to address this trade-off structurally。

Structure

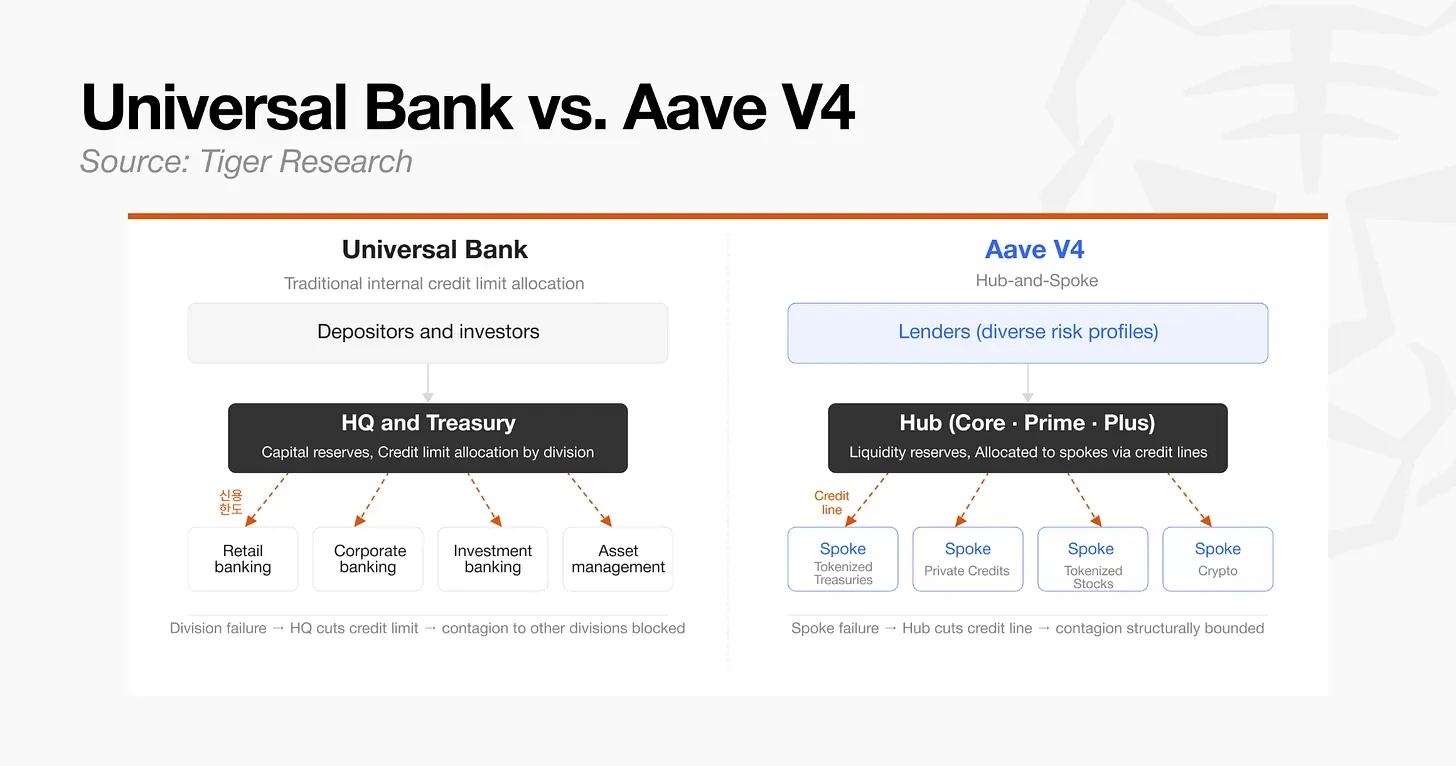

- Hub: Core level of consolidation of liquidity and accounting. It allocates lines of credit and debit lines to each branch, limiting the liquidity available in any given market. The basic risk firewall consists of these branch limits and local parameters。

- Spoke: An independent lending market with separate parameters for each asset. When problems arise with a branch or asset, governance and risk management personnel can reduce risk exposure by adjusting the credit lines of the branch, limiting additional borrowing or initiating emergency controls. The structural spread of the contagion effect is limited by design because the maximum risk exposure is fixed at the credit line ceiling。

In the traditional area of finance, this structure is similar to the internal credit line distribution system of a comprehensive bank. The Directorate-General allocates lines of credit to each sector and adjusts them to control spreads when a sector encounters difficulties. The hub plays the role of head office, while each branch functions as a separate business unit. Unlike the complete isolation model of Morpho, where capital is strictly locked in each asset pair, this central radiation structure allows unused mobility in one branch to be flexibly reallocated to more efficient branches through the credit lines of the central hub. The result is higher capital efficiency。

This structure has become a significant advantage in the RWA market. The emerging RWA market is often difficult to attract initial liquidity, but in Aave V4, existing liquidity centres can serve as seed mechanisms for new branch markets. By building tokenized assets into separate branches and capping the credit lines at the centre, the liquidity base of safer assets could be used to move new asset classes to the market at lower start-up costs, while keeping initial openings within the credit lines。

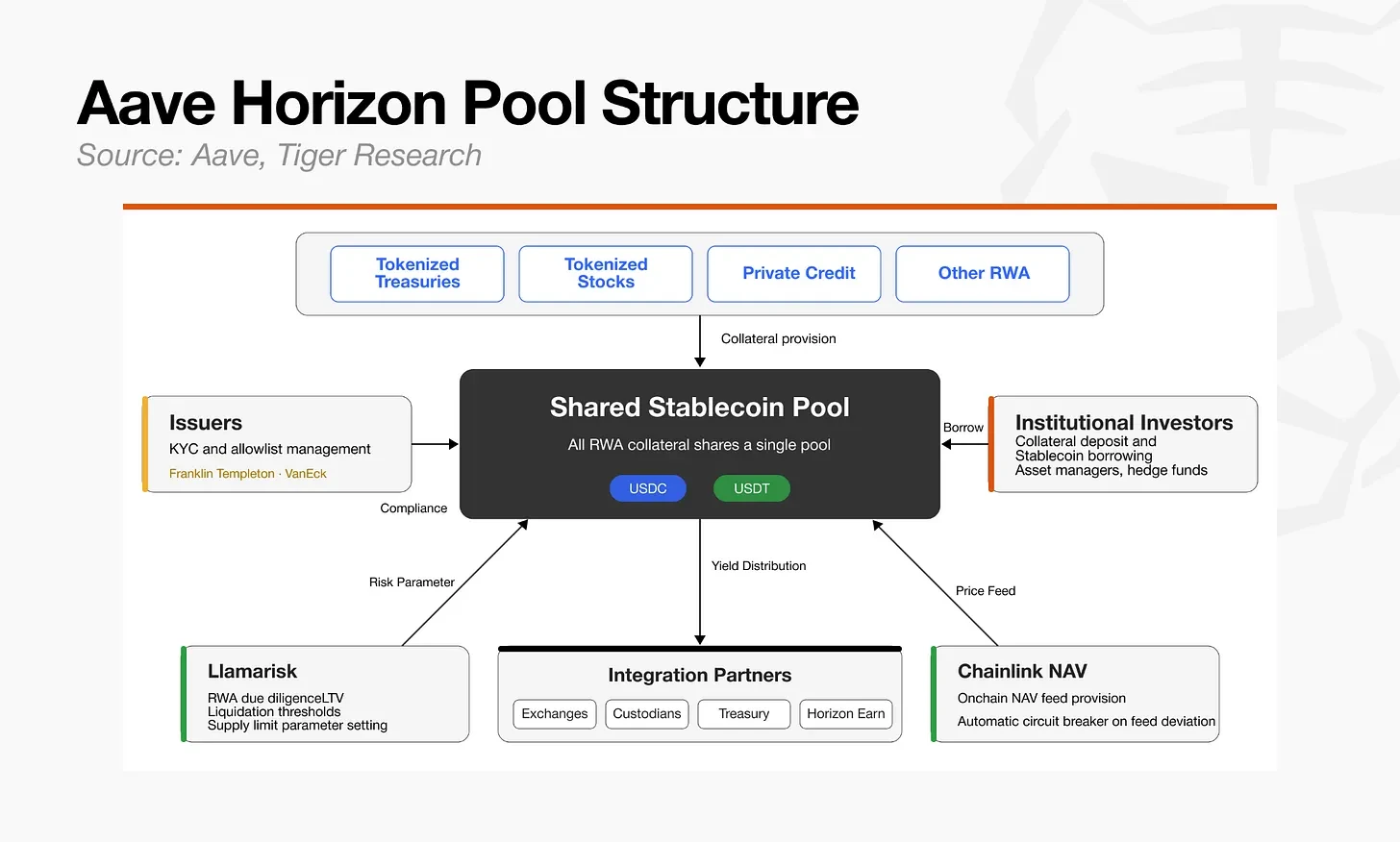

The institution uses mainly Horizon. Horizon was initially an example of an independent RWA loan based on Aave v3.3, but its design concept is consistent with the direction of the V4 unified liquidity and risk separation. With the deepening integration of Horizon with the V4 credit line structure, it is likely to be further integrated into the RWA layer of Aave 's institution。

Horizon aims to allow regulated national currency bonds, money market funds and institutional funds to serve as collateral for stable currency lending, with the possibility of extending to asset classes such as monetized stocks and ETF。

Since the approved institutional assets within Horizon are linked to the same institutional level of liquidity, any new RWA can immediately take advantage of existing stable currency liquidityI don't know。

Roles within the mobility layer are as follows:

- Issuer: INVESTOR ACCESS AND KYC/AML ALLOWING LIST MANAGEMENT。

- Risk Manager (LlamaRisk)RWA RECOMMENDATIONS FOR DUE DILIGENCE, RISK FRAMEWORK AND PARAMETERS。

- Chainlink: Provide chain price information。

- Agreement (Aave): Smart contract execution。

In the traditional Aave market, new assets require deliberations and voting by the DAO Governance Committee, which slows down the process. Horizon separates these responsibilities: the issuer is responsible for compliance with each asset, LlamaRicsk is responsible for risk due diligence and Chainlink is responsible for price validation. This structure allows institutional assets to go online and adjust risk much faster than all decisions are approved by the DAO Governance Committee。

Morpho minimizes governance participation and outsources market creation and risk management, choosing speed and choice, while Aave chooses different paths: controlling governance commissioning and sharing liquidity to maintain capital efficiency。

BOTH APPROACHES ARE CONSISTENT SOLUTIONS TO TRANSPOSE THE CONCEPT OF RISK ALLOCATION FROM TRADITIONAL FINANCE INTO A CHAIN ENVIRONMENT, BUT IT REMAINS TO BE SEEN WHICH SIDE THE RWA MARKET WILL EVENTUALLY APPROACHI don't know。

4.3 Euler V2: Multi-tactical hedge funds

In March 2023, Euler suffered $197 million in losses. The attack took advantage of a loophole in smart contract codes, with losses spreading to multiple assets as multiple asset markets were linked to the accounting and liquidation structure of the same agreement。

After approximately three weeks of negotiations, most of the stolen assets were recovered. Despite this, Eura chose to rebuild the architecture rather than merely repair, and subsequently repositioned itself as a flexible institutional lending infrastructure。

Euler ' s advance in the RWA and institutional credit market was driven by deficiencies in the monetization of traditional financial assets. Although banks issue monetized bonds, funds and national debt, these assets lack the chain infrastructure needed for loans or credit delivery。

Euler did not introduce institutional demand into the more volatile long-end encrypted asset market, but began to position itself as a credit base for institutional finance, providing chain liquidity for those assets。

Structure

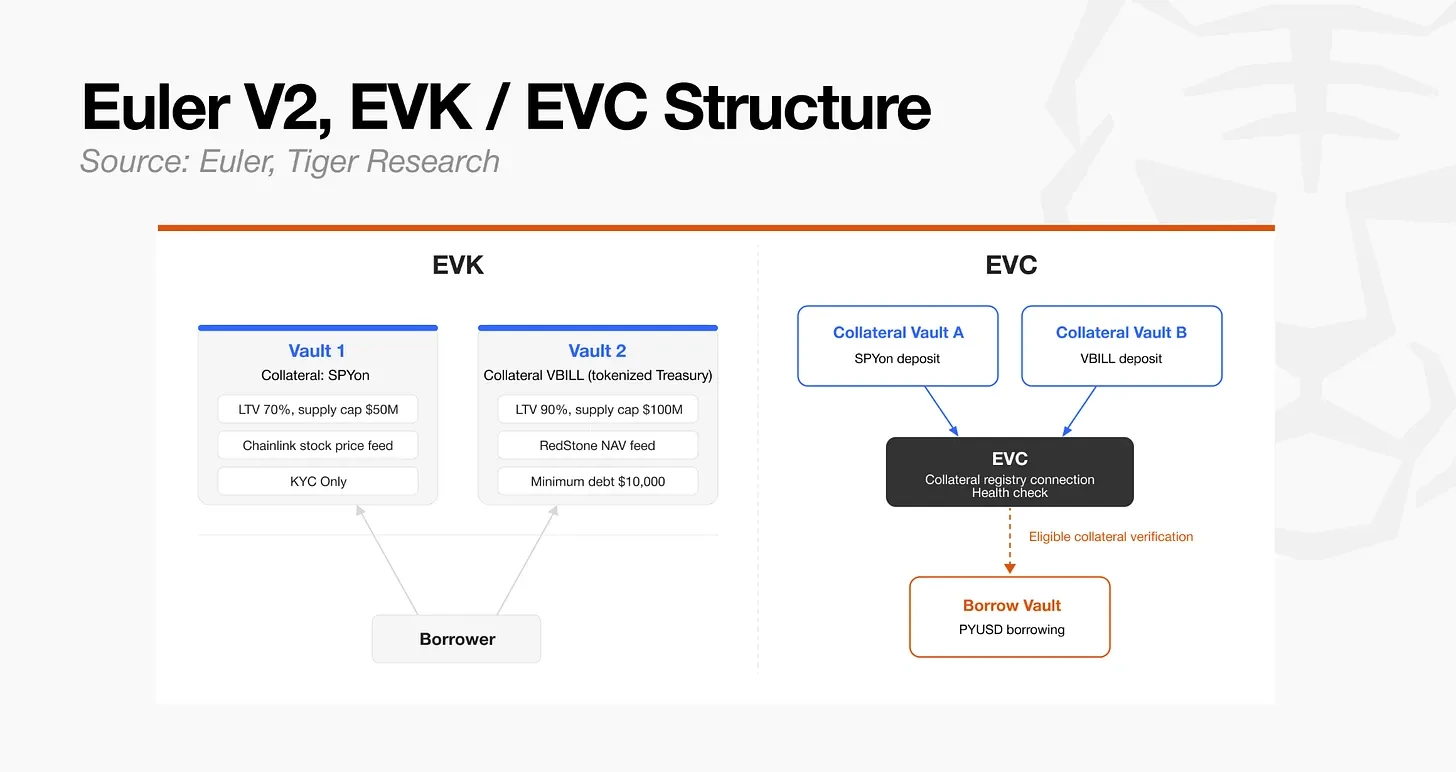

- EVK (Euler Treasury Suite): PACKAGE FOR CREATING ERC-4626-BASED CREDIT POOLS WITH LENDING FUNCTIONS. EACH VAULT CONTAINS STAND-ALONE PARAMETERS FOR THE ALLOCATION OF SPECIFIC ASSETS AND RISKS AND IS LINKED TO OTHER VAULTS THROUGH EVC TO FORM A LENDING MARKET。

- EVC (EXTREME TREASURY CONNECTOR)Core non-changeable language, used to connect collateral and debt relationships distributed in multiple vaults and managed in individual accounts. In traditional financial terms, it is similar to the consolidation of multiple decentralized asset accounts into a single bond account that provides cross-collateralization。

EVK ALLOWS FOR INDEPENDENT DESIGN AT THE ASSET LEVEL, WHILE EVC LINKS PREVIOUSLY DISPERSED ASSETS INTO A UNIFIED ACCOUNT AND POSITION MANAGEMENT FRAMEWORK。

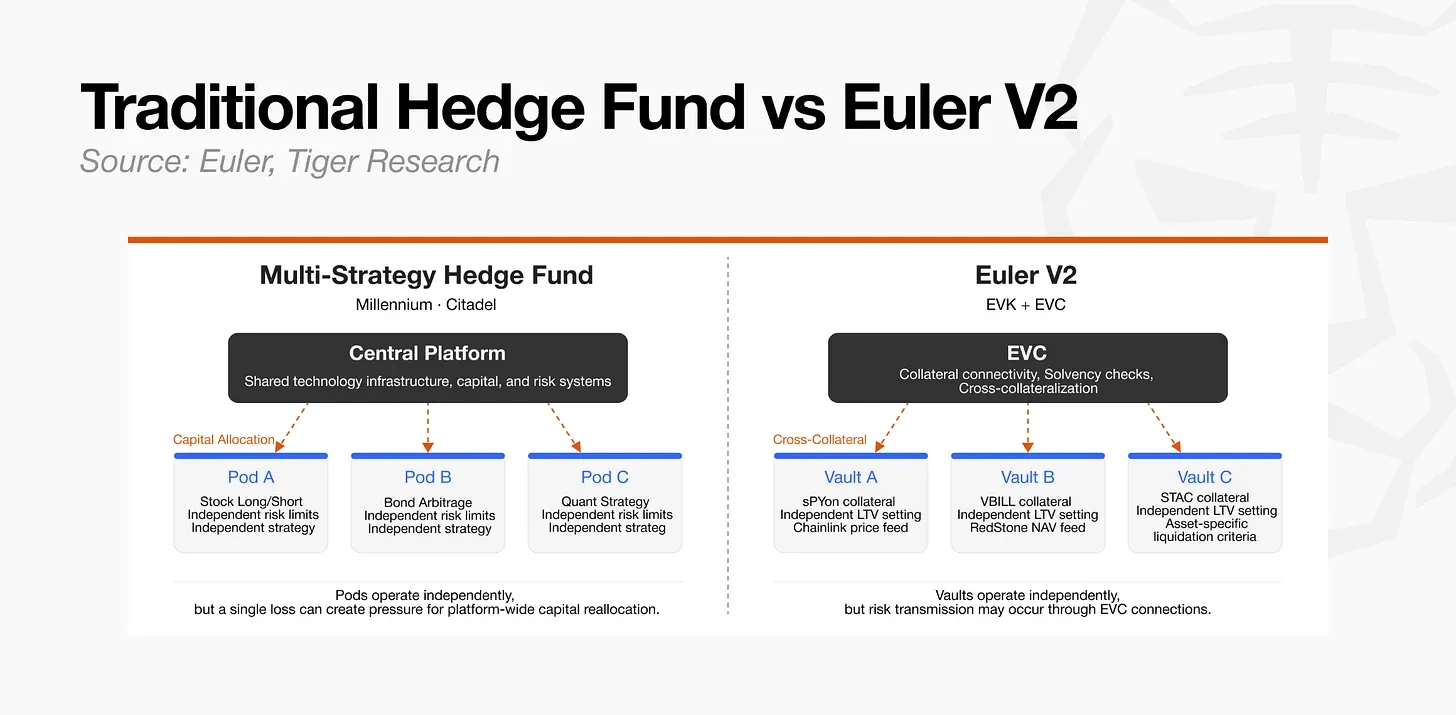

From a traditional financial point of view, the Euler Fund and the multi-strategy hedge fund “group” structure share some common features. Each independent team uses its own strategy and risk limits, while sharing technical infrastructure and capital management systems。

The key difference is that Euler is not an internal organization of the company, but an open infrastructure in which multiple independent participants can create and connect the vaults。

By analogy, if Morpho is similar to the division of labour model of the main broker, and Aave is similar to the shared liquidity model of an all-power bank, Euler is similar to the modularization structure of multi-strategy hedge funds. The flexibility and capital efficiency of such a structure also make it possible to transfer risks indirectly from one asset to another within the interconnected treasury ecosystem. As a result, the custodian risk management capacity remains a central challenge for the Euler V2 ecosystem。

Euler ' s institutional applications are moving towards adapting to asset characteristics and regulatory requirements. The primary objective is to monetize stocks. Equity assets are traded 24 hours a day, 5 days a week and require price information that reflects corporate events (e.g. dividends and stock splits). Under a single risk-sharing structure, it would be impractical to create an independent market that meets these conditions. This was achieved by allowing independent design at the asset level。

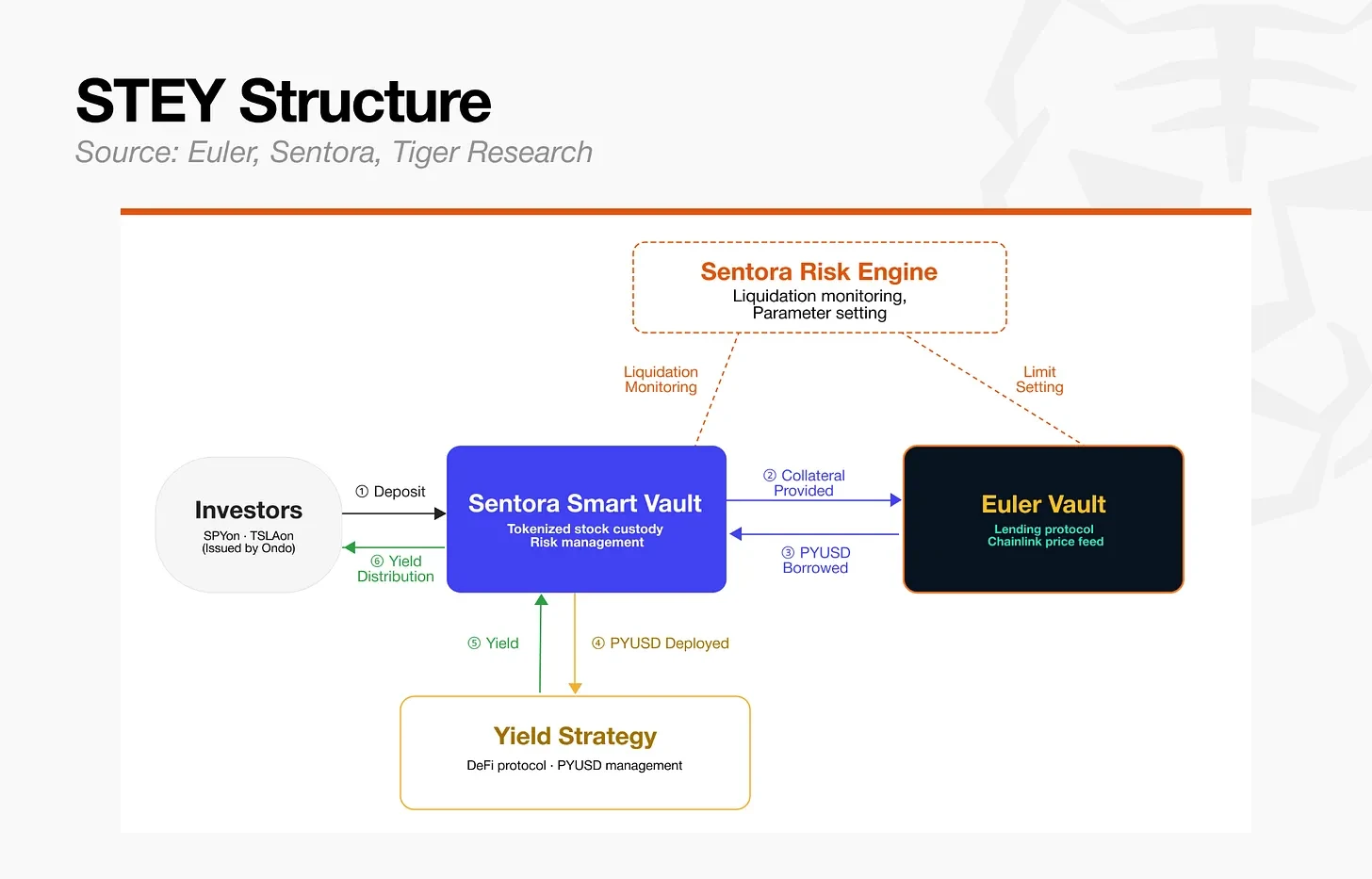

Euler, in collaboration with Ondo Finance, launched STEY, a lending market that accepts SPYon (Performance 500 index), QQQon (Nasdac 100 index) and TSLAon (Tesla) as collateral。

STEY MARKET STRUCTURE

- MortgageOndo monetized shares (SPYon, QQQQon, TSLAon)

- Loaned assets: PYUSD (PayPal stability currency)

- Price information: Chainlink Real-time stock price information

- Risk managementOther Organiser

JUST AS TRADITIONAL FINANCE USES LOMBARDI LOANS TO RELEASE THE LIQUIDITY OF STOCK HOLDINGS, THE STEY MARKET REPLICATES THIS MECHANISM IN THE CHAIN. INVESTORS CAN BOTH MAINTAIN PRICE EXPOSURES TO MONETIZED STOCKS AND CAN MAXIMIZE CAPITAL EFFICIENCY BY REDEPLOYING BORROWED SECURITIZED CURRENCIES TO CHAIN EARNINGS STRATEGIES。

The second aspect is the combination of monetized national debt and CLO (guaranteed loan certificate). Euler introduced KPK USDC Prime RWAVault to demonstrate this structural flexibility。

KPK USDC Prime RWAVault Structure

- MortgageVBILL (VanEck National Monetary Debt), STAC (Securitize AAA Level CLO)

- Loaned assets: USDC

- Price information: Redstone net daily information

- Risk managementOther Organiser

CLO NEEDS REGULAR NET VALUE PRICING THROUGH PREDICTIVE MACHINES AND FOLLOWING LIQUIDATION CRITERIA FOR SPECIFIC ASSETS. THE TREASURY REQUIRES STRICT COMPLIANCE CONTROLS. IN THE ABSENCE OF MODULAR INFRASTRUCTURE ALLOWING FOR THE CUSTOMIZATION OF INDEPENDENT INTERFACES AND PARAMETERS AT THE TREASURY LEVEL, IT WILL BE EXTREMELY DIFFICULT TO PUT THESE TWO ASSET CLASSES ON LINE AS COLLATERAL FOR BORROWING ON THE CHAIN。

Despite this, the potential for indirect risk transfer due to overlapping exposures to the same assets, prophecies and collateral remains, and Euler V2 faces the continuing challenge of balancing flexibility and control。

All three agreements address barriers to institutional access from different points of departure and approachesI don't know。

- Morpho• Full externalization of market creation and risk management to maximize speed and choice, with the quality of layers as key variables for validation。

- Aave• COMBINING CONTROLLED GOVERNANCE WITH THE CENTRAL RADIATION-TYPE STRUCTURE OF V4 AND PURSUING A HYBRID APPROACH THAT MAINTAINS CAPITAL EFFICIENCY WITHOUT COMPROMISING STABILITY。

- Earl: SEEK AN OPTIMAL BALANCE OF RISK IN A MULTI-STRATEGY STRUCTURE USING EVK AND EVC WHILE ENSURING SINGLE ASSET INDEPENDENCE AND CROSS-COLLATERAL FLEXIBILITY。

Their approaches vary, but they are moving in the same direction: separating the underlying implementation infrastructure from the risk judgement and designing asset-specific risk parameters for each type of collateral。

Conclusions

In traditional capital markets, it has taken decades for the primary broker to establish its position as the core infrastructure of hedge funds, covering all aspects of transactions, hosting, clearing, leverage and risk management. Following the collapse of Lehman Brothers in 2008 and the run-off of reserve-level funds, which exposed different types of systemic risks, the market increased its focus on hosting, collateral, liquidity management and role segregation。

DeFi has a structurally similar conclusion to make in a shorter period of time. It has been able to develop so quickly because codes are more iterative than regulation。

The early risk-sharing architecture suffered from governance bottlenecks and experienced unexpected risk exposures and the spread of bad debts, and Morpho, Aave and Euler were able to move quickly towards chain-based risk segregation and operational separation. Through repeated real capital losses and structural reconstruction, DeFi markets have completed the process of traditional finance in just a few decades。

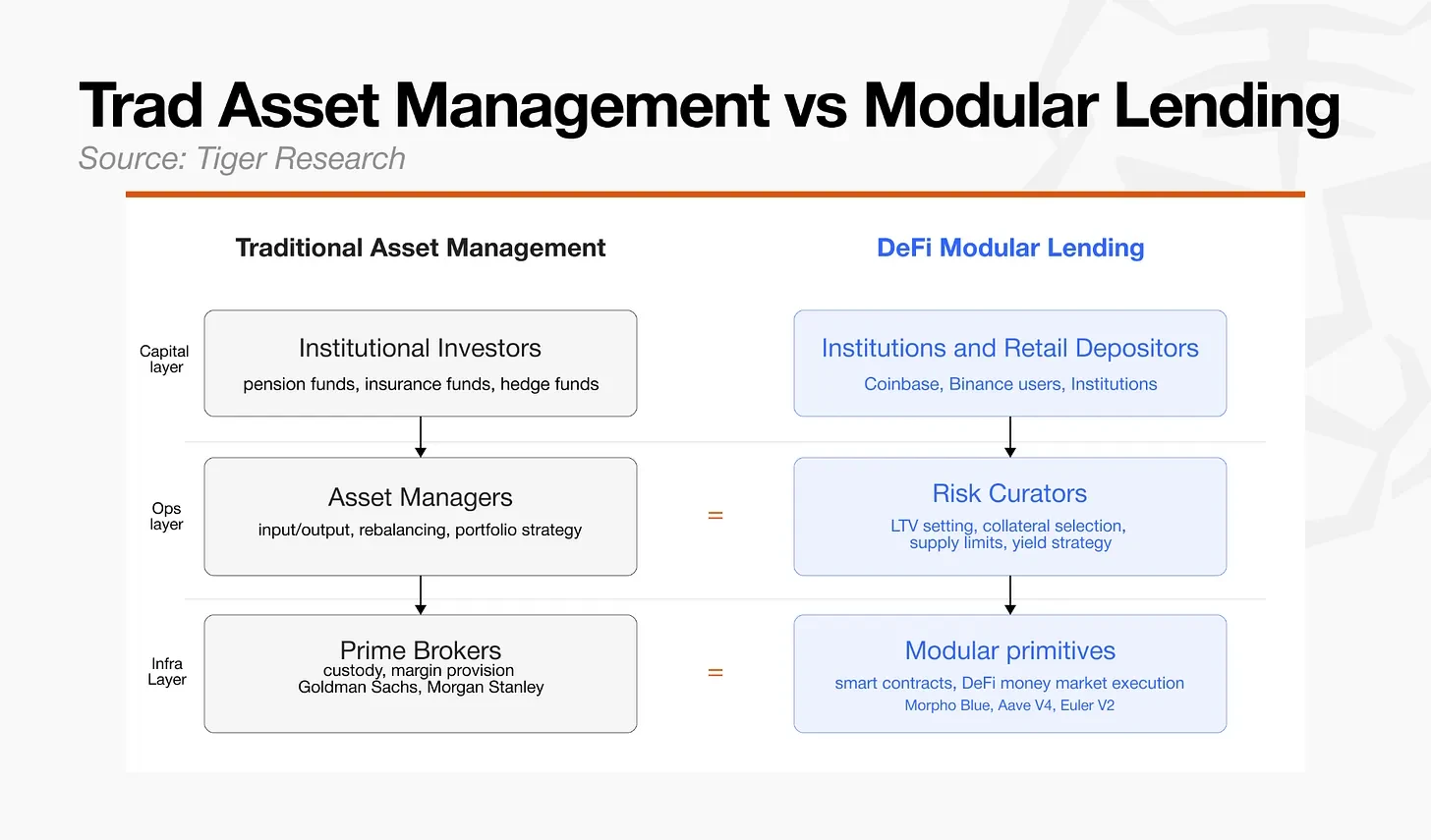

Traditional financial history shows that the maturity of infrastructure, such as brokering, is one of the conditions for the development of hedge fund industries. After 2008, with the stabilization of infrastructure and the onset of institutional capital inflows, the total asset management of hedge funds was close to $2 trillion. Between 2015 and 2025 alone, the size of the industry increased from $1.4 trillion to $4.5 trillion. As infrastructure matures, real competition in strategy and risk management begins at the upper operational level, and fund managers who demonstrate excellence attract market capital。

The chain lending market is entering a similar turning point. As Morpho, Aave V4 and Euler V2 converge on risk segregation and operational separation, the central issue today is what competition will occur at the operational level above these infrastructure。

At present, the total asset management of the chain treasury is approximately $7.4 billion. Given the rapid growth of the hedge fund industry after the infrastructure was built, the chain credit market is now more likely to be in the early stages of a larger expansion。

In the traditional area of finance, Goldman Sachs and Morgan Stanley have virtually monopolized the infrastructure of the primary brokers, and hedge funds must accept their terms in order to obtain access. The chain infrastructure operates differently. The opening of a market in Morpho or Euler does not require permission from any agency。

As infrastructure monopolies are broken, competition at the operational level of the chain is likely to take place more openly and rapidly than in traditional financial areas. In traditional markets, platforms such as the Bridge Water Fund, the Millennium Investment Group and the Castle Investment Group, as well as alternative asset management companies such as the Blackstone Group and Apollo Global Management, have attracted significant funds based on their operational capacity and infrastructure advantages。

On the chain, any participant capable of assessing collateral, designing risk parameters, responding to institutional regulatory requirements and establishing performance records now has an opportunity to take a place in emerging credit markets, with infrastructure that is much easier to provide than traditional finance。