WHO SHARED YOUR AI MONTHLY FEE? A MAP TO BREAK DOWN THE 20-DOLLAR ALGORITHM SUPPLY CHAIN

Income from AI applications is not equivalent to traditional SaaS, and corporate valuations depend on lower costs and improved Maori. 。

TL;DR

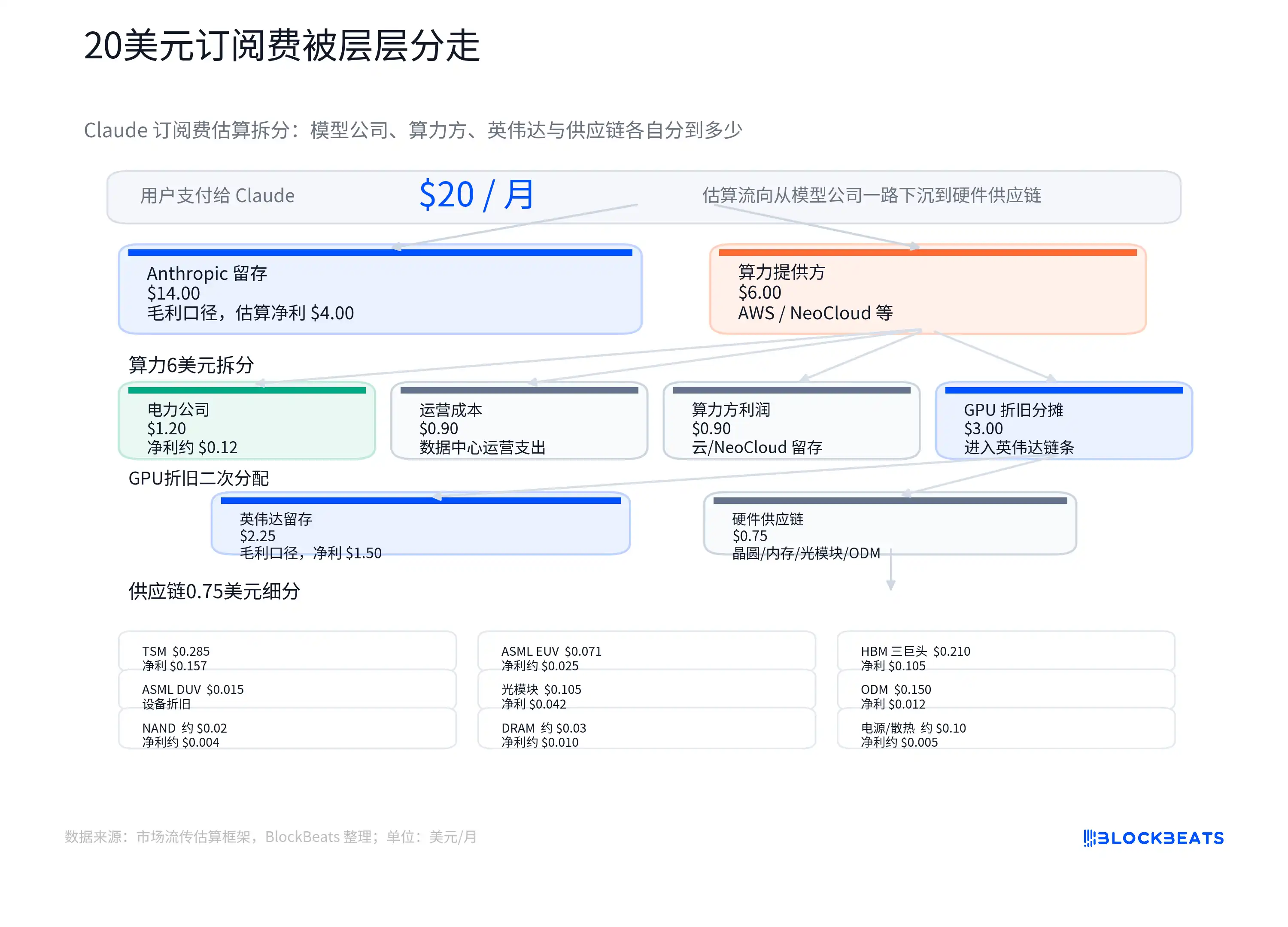

- Claude $20 subscribes to a cost-disaggregation map to disassemble an AI monthly fee to model companies, cloud computing, GPU, electricity and supply chains。

- AI Subscriptions have ongoing reasoning costs and cannot be directly applied to the traditional SaaS scenarios。

- Linked targets are: OpenAI, Anthropic, Microsoft, Amazon, Google, NVDA, Radio Accumulation, SK Hercules, Samsung, Light, Data Centre and Power Chain。

An estimate of how Claude Pro paid approximately $20 per month by the United States to model companies, cloud computing, GPU depreciation, electricity and supply chains is leading investors to revisit how AI applied revenue should be valued。

This figure is not an official sub-count for Anthropic, Amazonian cloud or Weeda, nor can it be considered a true book book of any company. Its value lies in raising a more fundamental question: how many subscriptions are paid by users for AI applications, and how many are deposited as much as traditional SaaS into software maturities

The traditional SaaS valuation is clearly imagined. Once the software is written, one additional account is sold, and the cost of new additions is usually low, and mature pure software companies tend to have more than 70% or more of their own. Investors are willing to give a multiple because of the opportunity to continue to increase their profit margins as revenues expand。

The trouble with AI applications is that each time a user asks, writes a code, analyzes a file or calls ant, it consumes GPS time, electricity, memory bandwidth and cloud resources. The surface is a fixed monthly fee, but the bottom is a cost chain that varies with usage. Light users may be high Māori and heavy users can run successive missions within available amounts or associated tool packages, and costs may rise rapidly。

So the challenge of the $20 split is not how many dollars a company has taken, but whether the AI application revenue is naturally equal to SaaS's income. AI has to prove its value is multiple, not only that the user is willing to pay, but also that the use-weighted Maori ratio will continue to improve。

There's a chain of reasoning costs behind the subscription

AI THE BIGGEST DIFFERENCE BETWEEN SUBSCRIPTIONS AND SUBSCRIPTIONS TO REGULAR SOFTWARE IS THAT THE MARGINAL COST OF " ONCE IN USE " IS NO LONGER CLOSE TO ZERO。

In the traditional SaaS, a team opens an additional account and service providers also have server, passenger and bandwidth costs, which usually do not rise linearly with each click. What is really expensive is prior research and development, sales and acquisition. When products are scaled up, a significant portion of the additional income can be retained。

Large model products differ. User input questions, models generate answers, a process called reasoning, that is, the actual calculation of the model when it is called by the user. Token is the basic unit of measurement for model reading and writing. The more the user asks, the longer the context, the more complex the content is, the more the token and the more the algorithm is consumed。

This creates a contradiction between fixed subscriptions and convertibility. Claude Pro paid approximately $20 per month for the United States, and the price would be affected by the region, taxes and taxes, and anthropic adjustments. Users see fixed prices and model companies face very different usages. There are people who write mail and check information, and there are people who process long files, run code assignments or call more complex automated processes。

THE MARKET-SPREADING MAP ATTEMPTS TO VISUALIZE THE MATTER: OF THE $20, A PORTION WAS LEFT TO MODEL COMPANIES, AND A PORTION WAS PAID TO CLOUD AND CALCULATOR PROVIDERS. THE CALCULATION COST INCLUDES ELECTRICITY, TRANSPORTATION, GPU DEPRECIATION. GPU PROCUREMENT FLOWS UPWARDS TO BRITISH WEEDA, POWER BUILDERS, HBM (HIGH BANDWIDTH MEMORY), LIGHT MODULES, ODM AND POWER-RELATED ENTERPRISES。

THE TERM "GPU DEPRECIATION" HERE IS UNDERSTOOD TO MEAN THAT EXPENSIVE GPUS ARE NOT A ONE-TIME COMPLETION BOOK, BUT ARE SLOWLY DISTRIBUTED TO AI SERVICES IN TERMS OF AGE, INTENSITY OF USE OR ACCOUNTING CALIBRE. THE TRUE DISTRIBUTION IS AFFECTED BY THE SIZE OF THE PACKAGE, THE PROPORTION OF LIGHTWEIGHT USERS, THE INTERNAL SETTLEMENT PRICE OF THE CLOUD MANUFACTURER, THE ALLOWANCE DISCOUNT, THE UTILIZATION OF THE GPU AND THE AGE OF DEPRECIATION. NOR ARE AVERAGE COSTS EQUAL TO MARGINAL COSTS。

INVESTORS REALLY NEED TO FOCUS ON THE DIRECTION: AI IPS CANNOT ONLY DISCLOSE INCOME GROWTH, BUT ALSO ANSWER WHETHER THE CALCULUS COSTS BEHIND INCOME GROWTH ARE INCREASING SIMULTANEOUSLY. MĀORI PRESSURE MAY BECOME MORE PRONOUNCED IF USAGE EXPANDS FASTER THAN MODEL EFFICIENCY INCREASES AND THE HIGHER THE SUBSCRIPTION INCOME. ONLY WHEN EFFICIENCY IMPROVEMENTS ARE FAST ENOUGH WILL MODEL COMPANIES HAVE THE OPPORTUNITY TO REGAIN ACCESS TO THE PROFIT STRUCTURE OF SOFTWARE COMPANIES。

Infrastructure receives a more definite income first

AT THIS STAGE, AI USAGE GROWTH FLOWS MORE DIRECTLY TO INFRASTRUCTURE THAN TO THE ENTIRE APPLICATION LAYER。

Whether the user uses the model in Claude, ChatGPT, Gemini, or within the enterprise, an individual, the reasoning eventually falls into computing, electricity, memory and network. There may be a turnover of products at the application level and a more rigid consumption of bottom resources. As long as AI usage continues to rise, cloud capital expenditure, GPU procurement, HBM demand and data centre electricity will be pulled。

THIS IS ALSO WHY INFRASTRUCTURE CHAINS SUCH AS IN WEIDA, TELECOMMUNICATIONS, AND SK HERCULES CONTINUE TO BE REVALUED BY THE MARKET. THE OVERALL MĀORI RATE IN YINGWEIDA HAS BEEN HIGH IN RECENT YEARS, WITH THE GAAP AND NON-GAAP MĀORI RATES OF APPROXIMATELY 71.1 AND 71.3 PER CENT FOR THE YEAR 2026, AS WELL AS THE SUBSEQUENT QUARTERLY GUIDELINES. IT NEEDS TO BE NOTED THAT INDIVIDUAL QUARTERS ARE DISTURBED BY SPECIFIC COSTS AND THAT PUBLIC FINANCIAL DISCLOSURE DOES NOT ALWAYS REMOVE THE REAL MAORI STRUCTURE OF THE AI DATA CENTRE DIRECTLY, BUT THE EXISTENCE OF PRICING RIGHTS FOR SCARCE INFRASTRUCTURE IS REFLECTED IN PERFORMANCE。

HBM IS THE MOST TYPICAL LINK IN THIS CHAIN. IT'S NOT AN ORDINARY MEMORY, IT'S A KEY COMPONENT IN THE AI ACCELERATOR THAT SUPPORTS HIGH-INPUT CALCULATIONS. THE INCREASED DEMAND FOR MODEL SIZE, CONTEXT LENGTH AND CODING LEADS TO GREATER DEPENDENCE ON HIGH BANDWIDTH MEMORY FOR AI CHIPS. SUPPLY CHAIN ESTIMATES SHOW AN INCREASE IN HBM ' S SHARE OF THE COST OF A NEW GENERATION OF AI CHIPS, WHICH IS ALSO AN IMPORTANT REASON WHY SK HERCULES, SAMSUNG, AMERICAN LIGHT WAS REPRICING IN AI CYCLES。

electricity and data centres have also moved from background costs to investment hubs. the energy consumption of a single regular text query is not necessarily exaggerated, but complex agents, context, code generation and multiple rounds of tasks are magnified. for cloud manufacturers and data centre operators, the key is not to ask how much electricity is consumed at one time, but to ask how much reasoning requests continue, cluster utilization, electricity prices, cooling, room capacity and grid access capacity become costs and bottlenecks。

THE ADVANTAGE OF THE INFRASTRUCTURE END LIES IN FASTER PERFORMANCE VALIDATION. AI CAPITAL EXPENDITURE BY CLOUD MANUFACTURERS HAS ALREADY TAKEN PLACE, INCOME AND MAORI FROM INGWEIDA IS REFLECTED IN THE FINANCIAL STATEMENTS, AND HBM COMPANY ORDERS AND PRICES WILL ENTER THE PROFIT STATEMENT RELATIVELY QUICKLY. MODEL APPLICATION LAYERS ARE TRADED MORE IN ANTICIPATION OF THE FUTURE: SUBSCRIPTION CONVERSION, BUSINESS PENETRATION, PROFIT RELEASE AFTER API INCOME AND FUTURE COST CURVE DECLINE。

Efficiency improvements remain a central and multifaceted basis

SOFTWARE INVESTORS AND AI MULTIPLE HEADS ARE NOT WITHOUT REBUTTAL. THE CENTRAL POINT OF EFFICIENCY IS THAT TODAY ' S HIGH COST OF REASONING IS ONLY AN EARLY-STAGE PHENOMENON AND THAT MODEL OPTIMIZATION, CACHES, SMALL MODELS, SELF-STUDY CHIPS AND HIGHER CLUSTER UTILIZATION CAN CONTINUE TO REDUCE UNIT COSTS. AS LONG AS COSTS FALL FAST ENOUGH, AI APPLICATIONS MAY STILL RETURN TO THE HIGH-MĀORI SOFTWARE LOGIC。

This rebuttal has a realistic basis. Some of the mainstream models have experienced a marked decline in unit prices with equal or higher capabilities. OpenAI has previously disclosed that GPT-4o Mini is 99% lower than the early text-davinci-003 cost per token. The rhythms of different companies are not entirely consistent, and Anthropic has more recently been reflected in price upgrades and model layers, but the industry direction remains to provide stronger capabilities at lower cost。

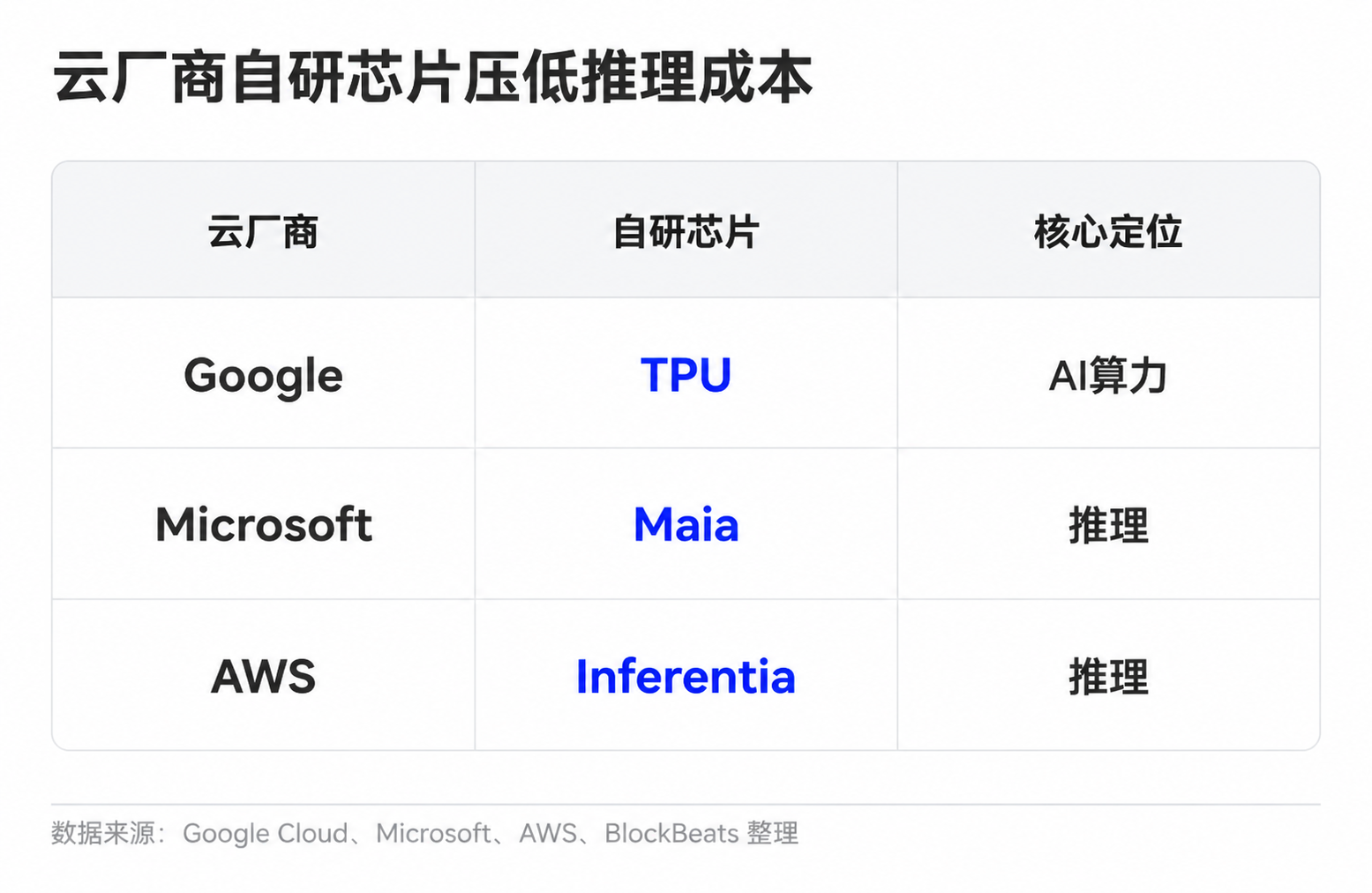

Model companies also have a variety of ways to improve unit economy. Simple tasks are given to small models, and frequent requests are sent to stronger models through cache reuse, long context and complex tasks. Cloud manufacturers reduce unit computing costs through self-study chips and cluster movements. Google has TPU, Microsoft has launched Maia for reasoning, and Amazon is pushing Trainium and Inferentia。

THERE IS ROOM FOR IMPROVEMENT IN AI APPLICATION OF PROFIT MARGINS IF IT IS BASED SOLELY ON TECHNOLOGICAL ADVANCES. CHEAPER REASONING, BETTER MODEL ROUTING, AND MORE COMPRESSIVE POWER MAKE THE SAME $20 SUBSCRIPTION TO CARRY MORE USAGE. LIGHT USERS, HIGH-PRICED ENTERPRISE PACKAGES, API LAYERS AND STRICTER USE LIMITS CAN ALSO IMPROVE OVERALL UNIT ECONOMY。

The difficulty is that cost reductions are not the only variable. AI application is moving from simple chat to a heavier task load. In the past, users may have been simply asking questions and rewriting texts, and there is now a growing demand from code agent, long document processing, video and multi-modular generation, and enterprise automation processes. These scenes are more valuable and consuming. The more useful the model is, the more likely the user is to entrust it with more complex and longer tasks。

DIFFERENCES BECAME MORE SPECIFIC: THE RATE OF DECLINE IN REASONING COSTS COULD EXCEED THE INCREASE IN USAGE AND COMPLEXITY OF THE TASK. IF UNIT COSTS FALL RAPIDLY, BUT AVERAGE CONSUMER CONSUMPTION INCREASES MORE RAPIDLY, THE MODEL COMPANY ' S WEIGHTED MĀORI RATIO WILL REMAIN UNDER PRESSURE. IN TURN, AI SUBSCRIPTIONS MAY MOVE AWAY FROM TODAY ' S HEAVY-COST FEATURES IF MODEL ROUTES, CACHES, SELF-STUDY CHIPS AND PRICE LAYERS ARE SUFFICIENTLY EFFECTIVE。

The number of subscribers is not a Maori rate

The United States dollar split map should not be understood as final. It is more like a valuation at the current stage that investors need to discount the assumption that "AI application is natural equal to SaaS" when the market does not yet see sufficiently transparent model company MUR rates。

For unlisted model companies such as OpenAI, Anthropic, it is difficult for external investors to see the full books. Financing materials, partner disclosures, cloud cost structures, enterprise package prices, API revenue share and use restrictions all serve as a point of appreciation. The truly valuable data are not the number of fee-paying users, but the share of light and heavy users, the willingness of business clients to pay higher prices for high-intensity use, the decline in cloud clearing costs, and the ability of unit reasoning costs to fall into corporate maturities。

THE CERTIFICATION OF THE LISTED COMPANY CHAIN WILL APPEAR IN THE FINANCIAL STATEMENTS MORE QUICKLY. THE GROWTH IN THE GROSS MĀORI RATE AND DATA CENTRE INCOME, THE DEMAND FOR ADVANCED DESKTOP POWER PRODUCTION AND CONTAINMENT, THE PRICE AND PROFITABILITY OF HBM MANUFACTURERS, AND THE INTENSITY OF CAPITAL EXPENDITURE BY CLOUD MANUFACTURERS WILL CONTINUE TO REFLECT WHETHER AI USAGE CONTINUES TO FLOW TO THE INFRASTRUCTURE END. IF THESE INDICATORS REMAIN STRONG AND THERE IS A LACK OF EVIDENCE OF IMPROVED MĀORI RATES AT THE MODEL APPLICATION LEVEL, THE MARKET WILL CONTINUE TO PROVIDE A MORE DEFINITIVE VALUATION PREMIUM FOR INFRASTRUCTURE。

Ultimately, to recover the higher valuation anchor, the model company needs to demonstrate that not only the user is willing to pay $20, but that these subscriptions, after heavy use, still leave enough Maori behind. The next round of pricing differences may well be different from the ARR ' s headline figures, while the reasoning costs, the package restrictions and the company ' s fee prices run simultaneously。