ONE HUNDRED DOLLARS AFTER FOUR YEARS, WILL THE PLAN FOR A PIECE OF SHIT COME TRUE?

The result will depend on where the flow of liquidity from the monetization wave ends. 。

Photo by Liam Akiba Wright

Original language: Luffy, Foresight News

TL; DR:

- It was reported that the Bank of Slags had published the Uniswap study, giving a target price of US$ 100 for 2030。

- The core logic of the slag is that tokenized assets will generate open DeFi liquidity needs, and Uniswap is expected to take over a large number of transactions and earn fees。

- However, most of the agency-level monetization products are made on an access basis, and the Belet Buidl products prove that barriers to access remain in DeFi tracks。

STANDARD CHARTERED BANK HAS SET THE TARGET PRICE AT $100 AT THE END OF 2030 FOR THE UNI TOKEN, WHICH MEANS THAT THE HEAD OF THE TRANSACTION GOES TO THE CENTRAL EXCHANGE FOR THE MANAGEMENT OF THE COIN, WHICH IS FAR ABOVE CURRENT MARKET PRICES。

The slag argued that future monetized assets of various types would require decentralised trading platforms that would transform financial instruments along the fragmentation chain into negotiable liquidity。

The slag calculates that by 2028, the total global monetized asset size will have reached $4 trillion; by 2030, the share of monetized asset inflows to the DeFi market will have risen from about 3.5 per cent to 30 per cent at present. Based on that estimate, the size of the assets carried in the DeFi market is expected to exceed $2 trillion in 2030。

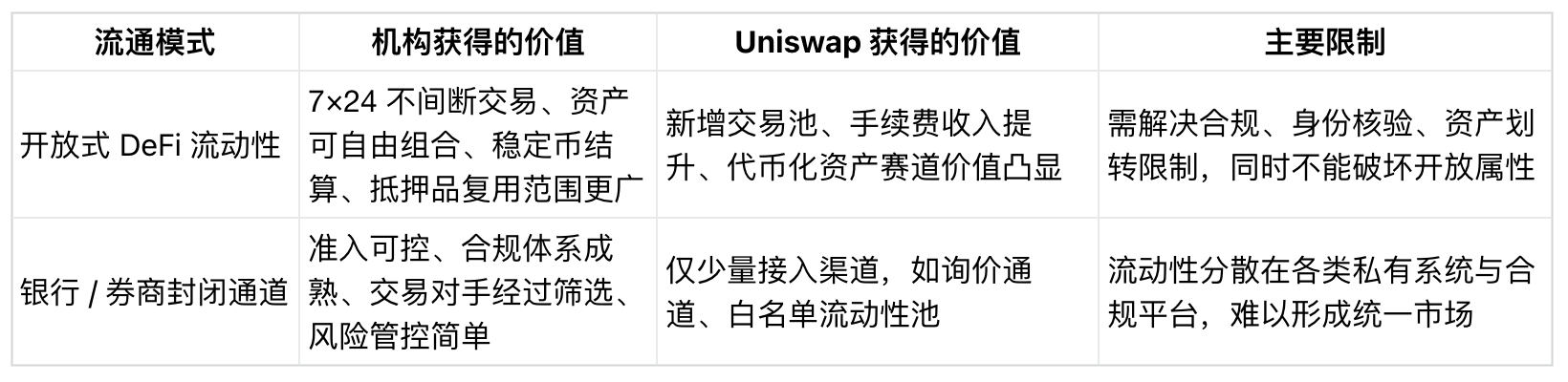

Banks, regulators, transfer registration service providers and compliance platforms are all set up on the monetization track. However, an open decentrization agreement would cover the liquidity dividend if such assets required the ability to be traded 24 hours a day, flexible collateral, cross-product combination and could not be met by a single agency-owned system。

Based on the current market environment, the core of the industry's doubts surfaced: whether assets in the chain, such as national debt coins, fund tokens, stock tokens, stable currencies, would be the liquid target of an open decentralized market, or would they always be restricted to circulation within a closed system with strict access and transfer to full control

Growth prospects depend on open liquidity

The valuation target given by the slag is based on a layered assumption: first, a substantial expansion in the size of the monetized asset market; secondly, a significant portion of the monetized asset is no longer merely chain-based, controlled assets, but is actually active in the DeFi market; and finally, Uniswap is able to take a sufficiently large share of related transactions, leading to an increase in the value of the UNI currency. At the heart of the logic, the focus shifted from the asset distribution to the liquidity transaction chain。

The monetization of assets has long been defined as a major long-term opportunity. In 2024, the Bank issued a joint report with the consulting firm Synpulse predicting that the global real-world asset monetization scale would be $30.1 trillion in 2034, with trade finance as one of the core applications. At the same time, the report mentions that monetization will lead to new DeFi applications and business models。

Citicorp, in June 2026, issued a report on monetization that compared market size with the opposite constraints: The baseline scenario for the line projected $5.5 trillion in monetized assets in the 2030s, with an optimistic scenario of $8.2 trillion. The report also noted that hybrid models might dominate and that agencies would control distribution, distribution and settlement channels。

The dichotomy of the two routes directly determines the development space of Uniswap. Open DeFi will have very limited development space if tokenized assets continue to grow in size, but their value is always deposited within banking platforms, pass-through service providers systems, voucher networks and compliance trading markets。

On the other hand, the industry status of agreements such as Uniswap would be significantly enhanced if various kinds of monetized financial instruments, stable currencies, mortgaged assets required free trade across product lines。

The DeFiLlama data confirms that Uniswap has the basis for the demand. As at the time of the release, the total multi-chain warehouse volume of the agreement was approximately $2.89 billion, with close to 30 days of processing fees earning over $50 million。

The available data represent only the base operating scale, but are sufficient to demonstrate that Uniswap positioning is a liquid infrastructure。

There are clear ethical differences between the two institutions. The issue of fund tokens is a process that creates a place for transactions that allow for the free exchange of tokens and stable coins, collateral, other token assets and is another independent business。

The gap between the two determines whether automation as a marketer, Uniswap, can become an infrastructure requirement, or simply a bypass to the edge。

As a result, the choice of trading channels and the issuance of assets are equally important. Liquidity determines whether a monetized product can form a tradable market, reusable collateral, or a settlementable asset, otherwise it will become a static document of title within the compliance system。

Belet BuIDL: Connect to DeFi but build access gates

The Digital Liquidity Fund (DMF) of the Bélédé institution is a real case at hand. In February this year, Uniswap Labs and the Compliance Platform Securitize jointly announced that BIDL, the United States dollar agency, had landed on the UniswapX trading channel。

This correspondence is subject to the request-for-money transaction mechanism, which is open only to white-list users and pre-qualified participants。

CryptoSlate's previous reports on BUIDL point to a core contradiction: while the BUIDL holder can exchange USDC via UniswapX, there is a strict threshold for access to transactions。

While the transaction process is based on DeFi technology, the circulation of assets is limited to the institutional participants who pass the clearance。

THE REGULATORY MODEL IS FULLY REFLECTED IN THE INITIAL ISSUANCE RULES OF BELED BUIDL: THE PRODUCT IS INTENDED ONLY FOR QUALIFIED INVESTORS, WITH A MINIMUM START-UP VALUE OF $5 MILLION, AND ASSETS CAN ONLY BE TRANSFERRED TO PRE-APPROVED RECIPIENTS AND ARE NOT TRADED ON ANY EXCHANGE。

According to RWA.xyz, on June 16, the total assets of BUIDL were approximately $2.37 billion, with only 108 holders。

A combination of access rules would not be difficult to discern the current status of the monetization industry. Large-scale monetization products can be produced along the chain, but participation is highly centralized and managed throughout the process。

In May 2026, the investor road show material was also used as a case in which BUIDL access Uniswap was used to justify the use of decentralised platforms for asset distribution and trading。

Even if the full UNI valuation is not publicly available, the road show will be transferred to the enterprise digital asset support infrastructure, which is at the bottom of the $100 target price。

The Belet BuIDL model is in between, with the Uniswap technology being used at the bottom, but the access control of the reserved institutions is maintained throughout the process. The design provided a bridge to DeFi infrastructure, but did not place tokenized assets in an open pool without a threshold。

The liquidity option accepted by the agency ' s assets is expected to begin with a compromise model that relies on the DeFi infrastructure to complete the transaction and settlement, while imposing rigid restrictions on the identity of the user, the transfer of assets and the counterparty。

UNI STILL LACKS A VALUE CAPTURE MECHANISM

Even if Uniswap were to undertake more real-world transactions of monetized assets, it would not represent a direct benefit for UNI holders, and the agreement still lacks a stable value capture mechanism。

The UNI currency economic upgrading proposal, previously adopted by the community at the Tally platform, clarified the allocation of protocol fees, the UNI destruction mechanism and suggested that Uniswap should be the default trading hub for monetized assets。

This package provides a landing path for valuation logic, but there are multiple premises: community governance resolutions, adjustment of fees, institutional business cooperation, growth in real transactions。

THE SCUM CALLED FOR A TARGET PRICE OF $100, WHICH IS NOT ONLY FAR ABOVE THE CURRENT PATTERN, BUT EVEN BEYOND THE PEAK OF 2021. THIS OBJECTIVE CANNOT BE SUPPORTED BY GROWTH IN ASSET ISSUANCE ALONE, BUT MUST BE SUPPORTED BY REAL AND SUSTAINED TRADE FLOWS, STEADY REVENUE FROM FEES AND FEES, ALONG WITH CLEAR ARRANGEMENTS FOR DEVELOPMENT AND CURRENCY VALUE-LINKING MECHANISMS。

THE CENTRAL CONTRADICTION BETWEEN INSTITUTIONAL MONETIZATION IS THAT BANKS AND REGULATORY AGENCIES NEED THE ABILITY TO DECENTRALISE, INTER ALIA, CHAINED SETTLEMENTS, ROUND-THE-CLOCK TRANSFERS, PROGRAMMABLE MORTGAGES, AND STABLE CURRENCY PAYMENTS, WHILE AT THE SAME TIME INSISTING ON KYC IDENTIFICATION, ASSET TRANSFER RESTRICTIONS, THE DESIGNATION OF COUNTERPARTIES, AND AUTONOMOUS CONTROL OVER SECONDARY MARKET LAYOUTS。

This caution is also confirmed by the study on monetization conducted by the Financial Stability Board. The report indicates that the current global monetization is small, with multiple problems of closed access, inadequate inter-platform interoperability, restricted settlement assets and fragmentation of trading platforms。

These frictions are the central obstacle that prevents monetized assets from becoming a general defi liquidity marker。

If such industrial barriers persist, Uniswap will only become an associated interface on the margins of the institutional monetization system; if the pain is gradually eased, the agreement will become the central place for dealing with token funds, stable currencies, and home-grown and encrypted assets。

Ultimately, the core of this valuation forecast depends on where monetized liquidity ultimately goes. The target price of $100 represents considerable up-to-date space, and the more critical signal is that a traditional Wall Street launcher has endorsed the opportunity of the DeFi agreement to split the institutional monetization wave。

The Beled BUILL case has shown that the institution can use DeFi technology while maintaining strict mobility controls; the Citigroup’s vision of the monetization industry also suggests that Wall Street has a mixed system with distribution, distribution and delivery links firmly in the hands of the institution; and the various types of industry that the Financial Stability Board has suggested highlight that interoperability and settlement systems remain central to the industry。

Subsequent market signals will come from more cases of tokenized asset access. If all the new assets were to be placed on a segregated white list, open DeFi would be able to divide only a small part of the market; if the unified asset liquidity pool gradually landed, there would be fewer rules of self-defined control, and Uniswap would no longer be limited to the conversion of original encrypted currency。