The market value of 1.6 billion is only the opening: the real dividends of monetized stocks are built on the chain

Is it really a traditional capital coupling that's blowing up the dollar-denominated stock?

Ignas DeFi Research

This post is part of our special coverage Syria Protests 2011

I think there's only one way to make a lot of money on tokenized stocks。

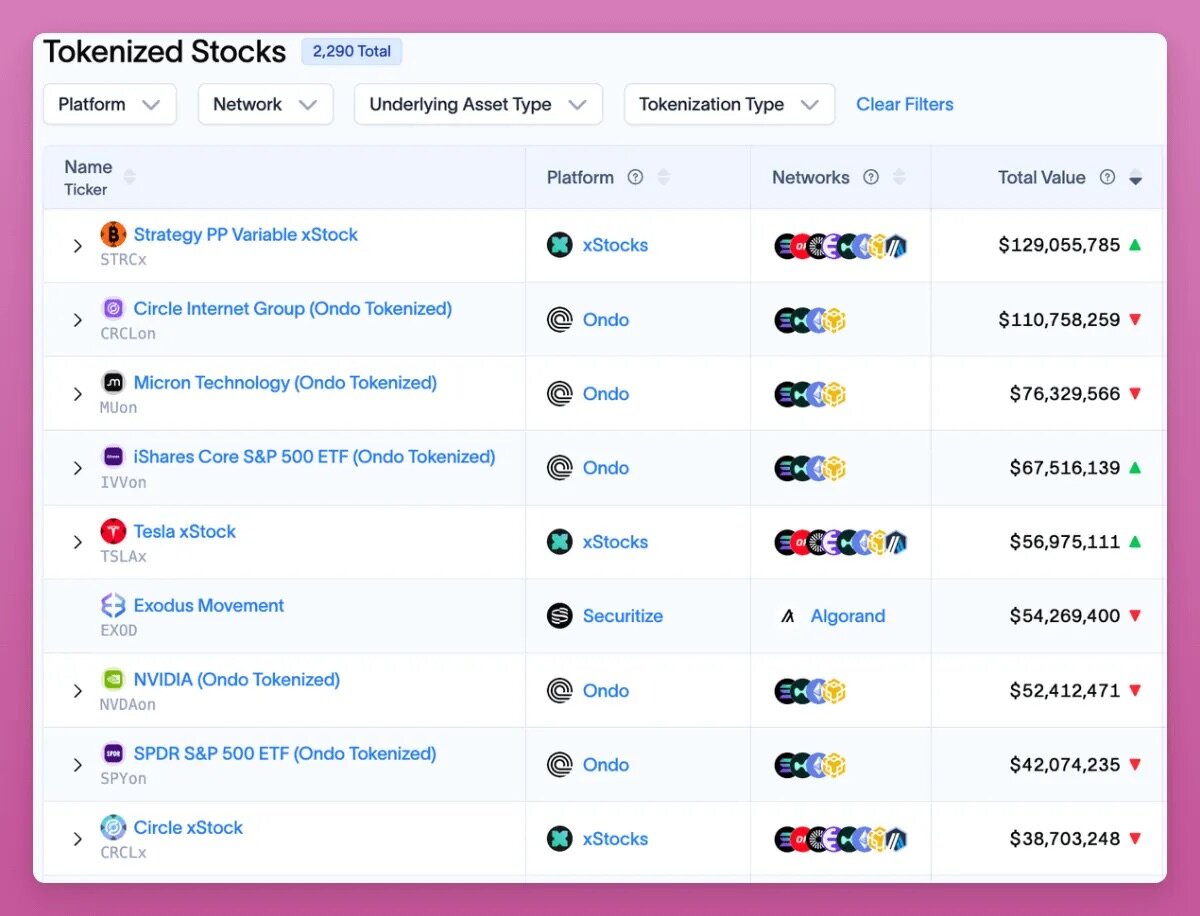

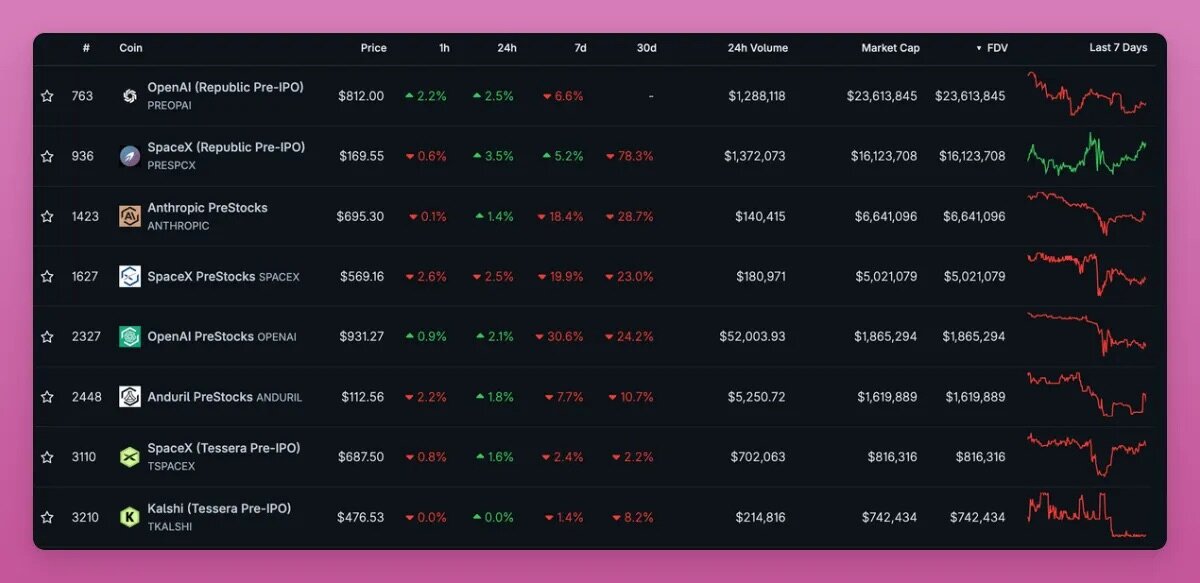

OF COURSE, YOU CAN BUY THIS KIND OF CURRENCY AND BET IT'S 10 TIMES HIGHER, BUT WITH VERY FEW EXCEPTIONS LIKE U.S.S.U., IT'S UNLIKELY TO BE RICH. FIRST, ONLY 2290 STOCKS ARE CURRENTLY MONETIZED, WITH A TOTAL MARKET VALUE OF OVER $1 MILLION ONLY ABOUT 130, AND THE VAST MAJORITY OF MONETIZED SHARES ARE BARELY LIQUID ON THE CHAIN。

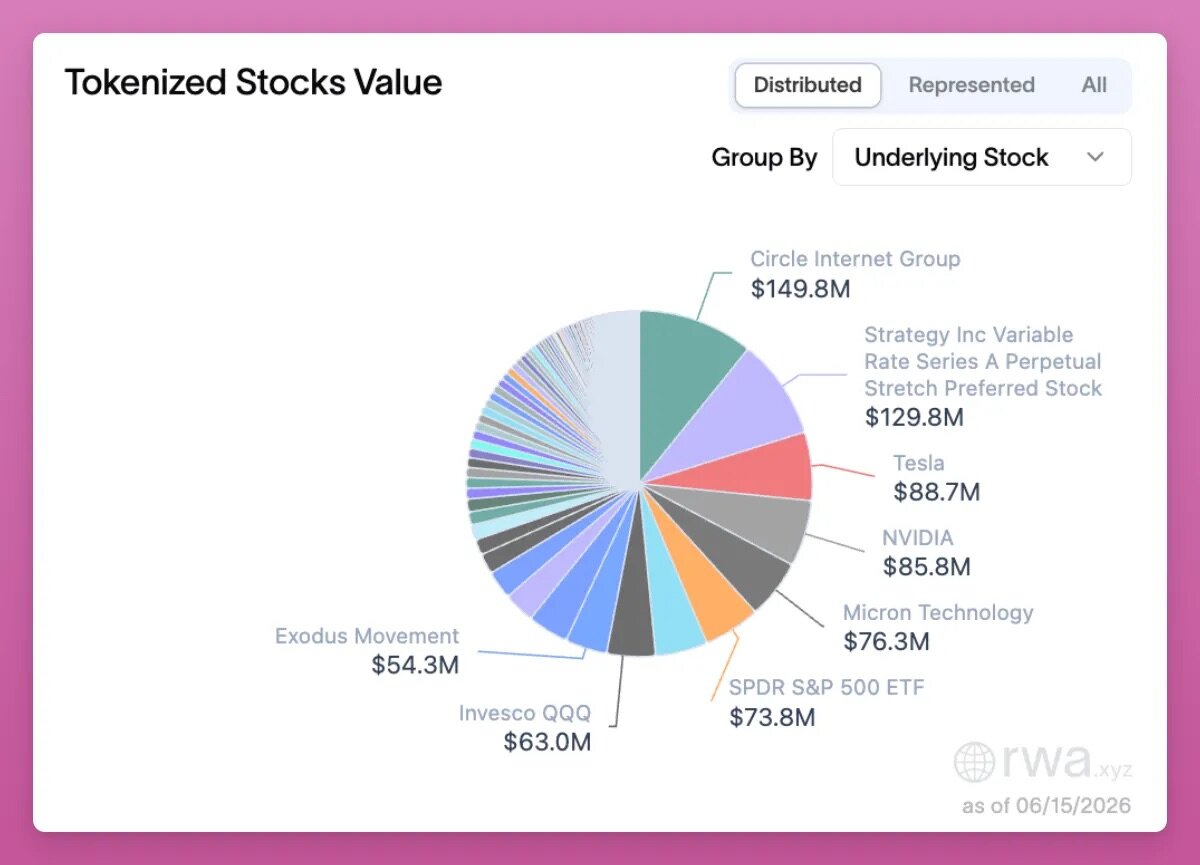

According to RWA data site rwa.xyz, Strategy is one of the largest targets, with a total value of $129 million。

It is now essentially mature corporate shares that have been traded, and if you want to dig into a stock that is undervalued and under-regarded by the market, traditional coupons, such as surplus securities, are more likely。

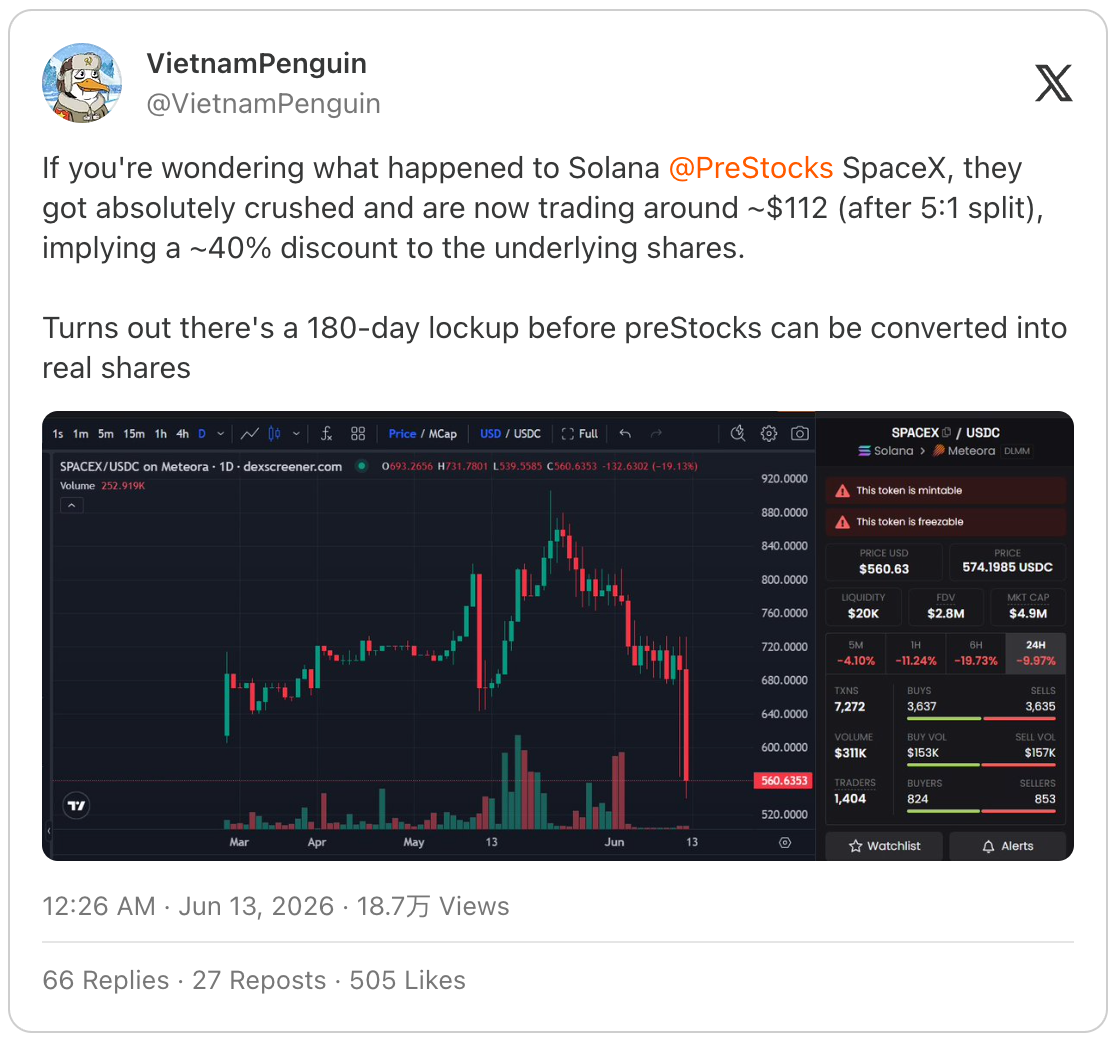

Second, holding token shares increases the risk that many traditional coupons do not exist. For example, investors who had purchased SpaceX token shares on PreStocks platform found that such tokens required locks for 180 days to convert into real stocks, which directly led to a 40 per cent drop in the price of the token。

Source: https://x.com/VietnamPenguin/status/2065470925252759680

Investors therefore bear the additional risks posed by issuers and asset custodians, in addition to the original smart contract risk in the encryption industry, the self-custody asset risk (and lack of self-custody), and the liquidity risk。

But I don't totally deny the monetization track. It's one of the most potentially rising plates in the encryption industry: It can attract new users and retain inventory users who intended to convert encrypted assets to traditional financial markets. Currencyization of shares brings chain-based transaction and transaction revenue to the block chain and can attract industry investment, developers and market attention。

The monetized stock itself holds many opportunities: you can deposit it in the Decentre Exchange (DEX) liquidity pool to earn a profit and use it as a collateral for borrowing; you can also hold the SPCX cash on the chain while opening a permanent contract, earning neutral benefits from delta and taking credit for the DEX platform。

Speaking of hedge tactics, you can buy currency-based stock spots and empty the Varial platform. The platform's original currency, VAR, is now probably the best air drop opportunity:

- 50% of the total supply of tokens will be allocated to the community

- The crediting exercise will end on 30 September, with only about three and a half months left for mining windows

- After the tokens went online, the team plan put out 30% of the platform battalion for buyback destruction

- The platform is still in closed testing。

Currencyization stocks are not part of the early investment track

But my biggest concern about tokenized stocks is that this track essentially makes encrypted investors the receiver of traditional financial assets。

The encryption industry was able to produce a large number of millionaires in the past because we pre-positioned a whole new track: bitcoin, smart contract chains, all kinds of project drops, NFT, Hyperliquid drops. SpaceX's tokenization listing process made it clear to me。

Its distribution patterns and two layers of encrypted tokens filled with heat are the same: small, completely diluted valuations, price increases and drops, and a complete disconnect between the basics of the enterprise. In the short term, traditional financial markets are now at a stage of "high and total underestimation of valuations" just like the encryption industry two years ago。

There is no denying that rockets, artificial intelligence, and chain operations sound promising, but corporate valuation, stock release schedules, data collection, and governance mechanisms can hardly be optimistic。

The core value of tokenization lies in broadening the distribution channels for assets: any user who owns a Phantom, Metamask, Rabby's wallet can hold such coins. It is less volatile than bitcoin, Shancocoin and is not a stable currency anchor in United States dollars, with risk gains between them. For investors outside developed markets, or for users who do not want or are unable to convert encrypted assets into traditional financial systems, monetization of stocks offers an attractive solution。

BUT THAT DOES NOT MEAN THAT WE GRASP EARLY INVESTMENT OPPORTUNITIES. THE CHARISMA OF THE ENCRYPTION INDUSTRY USED TO BE THAT IT GAVE ORDINARY PEOPLE IN THE DIASPORA THE OPPORTUNITY TO INVEST IN REVOLUTIONARY ENTERPRISES AT THE BEGINNING. THE IPO PROJECT, VALUED AT $2 TRILLION, COULD NOT BE DESCRIBED AT ALL AS AN EARLY LAYOUT。

The future of the encryption industry, which has real potential for long-term rises, is where firms have been coined in the stock chain since its inception. ICOs, fair distribution, was a good attempt, but in the last cow market cycle, the industry became more and more harvesty: early project private fundraising was too high, TGE was even higher, and the share of coins sold to the general public was too low. In his blog post, Cobie analyzed this very thoroughly。

I'm still investing in the Echo platform launched by Cobie, because it really offers early project investment opportunities: I've been involved in MegaETH ' s rotation, and the return on my investment has doubled 3.85 times, even though the currency goes online and the movement continues to fall。

Apptronic is a human robotic enterprise, and despite the high valuation, I'm involved in its B-wheel strategic financing. Such investment opportunities would not be open to ordinary diasporas。

By the way, in addition to Echo, I'm looking forward to the Legion platform, but it is not easy to dig into high-quality investment targets that are well valued and of too high quality。

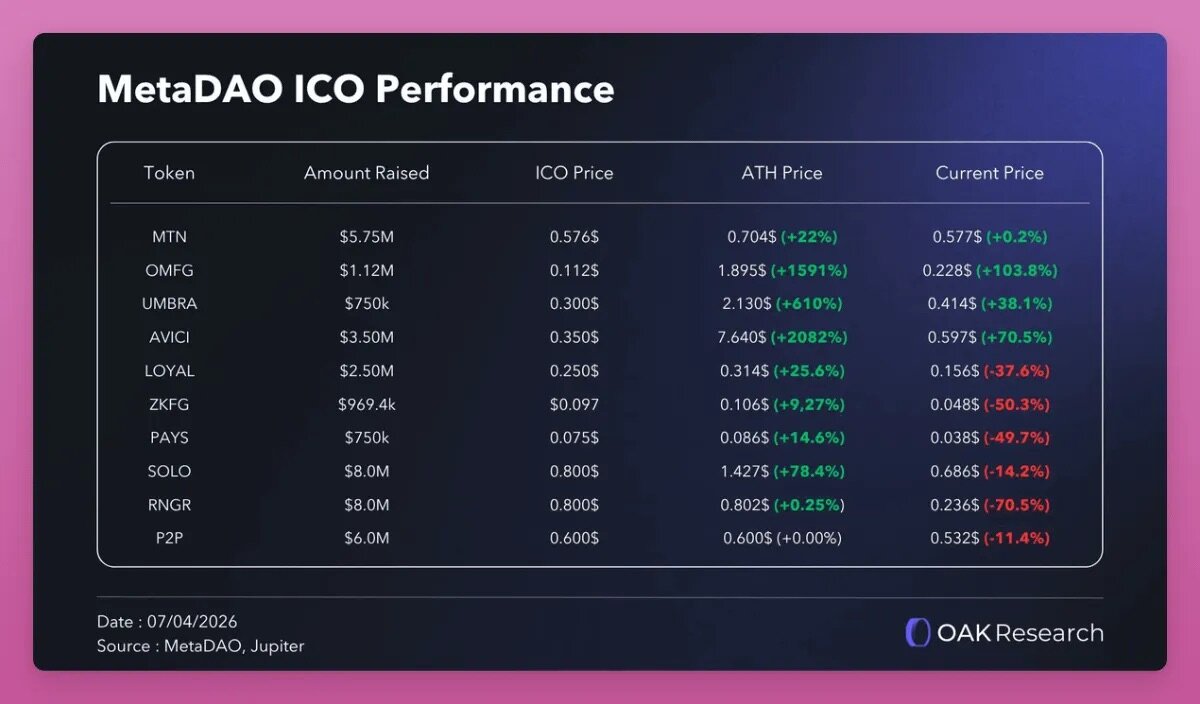

MetaDAO’s model is excellent: the issue of the Platform’s title token will give the holder a legitimate interest in controlling the treasury’s expenditure by a certain amount, while the unlocking of the coin, based on the company’s performance, will successfully address the core malfeasance revealed by its first issuance in the year. This is why, given the current market environment, the various ICO projects that are on line with MetadaO are performing relatively better。

Source: X Platform OAK Research

In addition to this, there are original chain distribution models, such as the Opening Bell product line launched by Superstate, the first target being Galaxy stocks, where business equity is issued directly。

Consider that if a large enterprise does not follow the listing process online, it issues its shares directly in the Taifung Solana public chain, rather than using only block chains to seal the legal documents. At that time, the non-removable, safe attributes of the block chain will become the core competitiveness of the industry, and the value of the tokens we hold will rise。

MetaLeX is the type of scheme: to create a fully programmable chain of enterprises, where capital, equity and equity are fully managed。

As a matter of fact, today the Centralized Exchanges of Money Ann, Coinbase and Kraken are all setting up traditional financial operations, including online stocks, bonds, and ETF token products. However, the XStocks platform was unable to deliver the underlying physical stocks, resulting in the complete de-advance of currency, Bybit, Bitget, and the non-performance of more than $1 billion of user orders. By contrast, the trading orders of traditional issuers are more secure。

The stabilization currency was initially used only for short-term asset storage, awaiting entry to encrypt primary assets; it is now a liquid export of capital from older investors in traditional finance。

Perhaps one would say that IPO ex-currencyization stocks allow ordinary people to pre-semble top star companies like OpenAI, Anthropic. Indeed, both are the most popular market-level tokens for the current market value, but the valuation of both enterprises is close to trillions of dollars。

This is hardly an early investment: Anthropic ' s latest H round of strategic financing has reached $965 billion. Financing rounds: A, B, C, D, E, F, G, H (last round)

It's still at an extremely early stage

The logic behind that is as follows: The Bank predicts that by 2030, decentralised intra-financial monetized assets will grow 37 times (currently only 3.5 per cent of total assets, rising to 30 per cent in 2030); the total monetized assets in the chain will have surpassed $4 trillion in 2028。

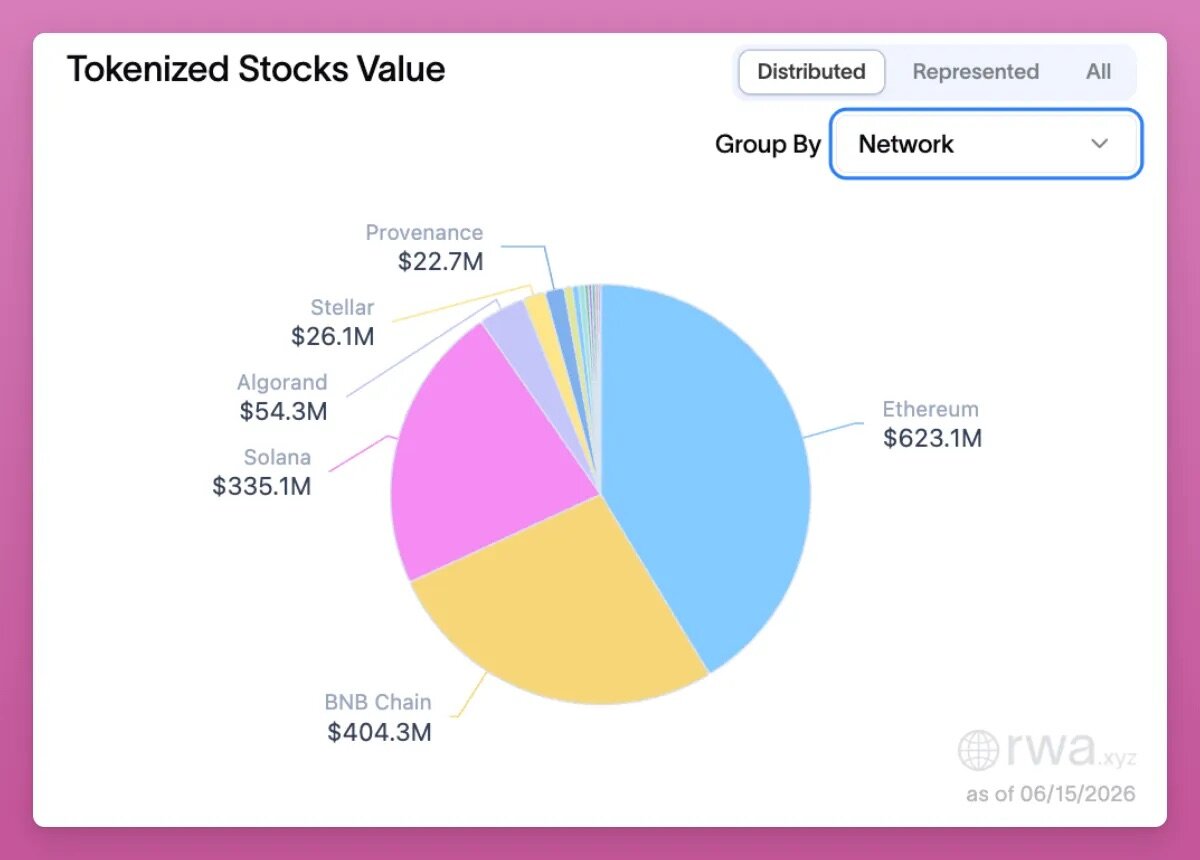

To date, the total value of monetized equity flows across platforms is $1.5 billion (such assets can be transferred from the distribution platform to the point between wallets), mainly deployed in the Ethershop, the BNB smart chain and the Solana public chain. But the total number of tracks remains small: $1.5 billion is even below the market value of the Uniswap token, the USI itself, of $1.9 billion。

THE SCUM HAS ALWAYS GIVEN EXTREMELY OPTIMISTIC PRICE FORECASTS (FORTICIPATED US$ 40,000 AND US$ 500,000 IN 2030 IN THE INN, BITCOIN), BUT THE BOTTOM LOGIC OF THE UNI IS VERY CLEAR: THE TOTAL VALUE OF THE DOLLARIZATION STOCK LOCKS CONTINUES TO RISE, LEADING TO HIGH TRANSACTIONS ON THE CHAIN AND A PARALLEL INCREASE IN PLATFORM FEES, WHICH ARE NOW USED TO BUY BACK AND DESTROY UNI COINS。

Not only did Uniswap benefit. The entire chain of encrypted industries will benefit once the monetization of equity lanes has broken out: the Aave, Fluid, Kamino Loan Agreement, and Pancakeswap, Jupiter and others, all of which will benefit from dividends。

The development of tokenization equity would give the encryption industry a counter-cyclical character: in the current decline in the price of bitcoin and tavern prices, decentrized lending would result in large-scale deleveraging, various agreements would shrink revenues and platform tokens would be charged simultaneously. The renewal of the contract to go to the Centralized Exchange was the first race to receive a tokenized stock dividend, and the latter will be the next wave of beneficiaries。

After the report was released, the UNI token went up 13 percent a day, but there were more investment opportunities on the track. In the last two weeks, Backpack's platform token BP grew by 200%。

Backpack, as a centralised exchange, has had difficulty finding the core business that really fits market demand, while competing with old brand-head exchanges like François and Hyperliquid to go to the centralised permanent contract platform to rob users. The monetization of asset operations seems to have finally led to a core growth path。

The vast majority of monetized shares on the market (xStocks, Ondo) are in the form of hosting seals: issuers hold physical shares, found currency to track stock prices, and users receive only price gains and do not have real equity. And Backpack made it available on the original chain through the Superstate Opening Bell product line: Such tokens are formal shares registered by the United States Securities and Exchange Commission and are fully consistent with the shares listed in NASDAQ, the holders of which have a share and voting right, and the platform holds a full set of compliance plates (the original team of Backpack was from the former FTX European Division)。

THIS LOGIC EXTENDS TO THE PLATFORM ' S ORIGINAL TOKEN BP: A PLEDGE OF BP FOR A YEAR CAN BE CONVERTED INTO AN ENTERPRISE ENTITY ' S EQUITY (SEVEN DAYS A YEAR FOR A FORECLOSURE WINDOW) WHEN THE COMPANY IPO IS ACQUIRED OR ACQUIRED。

There are also a number of direct trading opportunities on the monetization track: The Ondo industry is ranked second in terms of total negotiable value, and the platform has been issued with original currency ONDO。

HOWEVER, IN ADDITION TO ITS GOVERNANCE FUNCTIONS, THE ONDO HAS LITTLE VALUE CAPTURE CAPACITY, AND THE PLATFORM IS WHOLLY OWNED BY THE COMPANY AND WILL NOT BE DISTRIBUTED TO CURRENCY HOLDERS. WHILE THE MARKET IS DISCUSSING THE OPENING OF A FEE-SPLITTING MECHANISM, THE LANDING VARIABLE REMAINS. AND IN 2029, ALMOST 50% OF THE TOKENS WERE WAITING TO BE UNLOCKED。

IF THE MOOD IN THE CURRENCY STOCK MARKET GETS WARMER, SHORT-LINE ONDO EXISTS, BUT I WON'T HOLD IT FOR LONG。

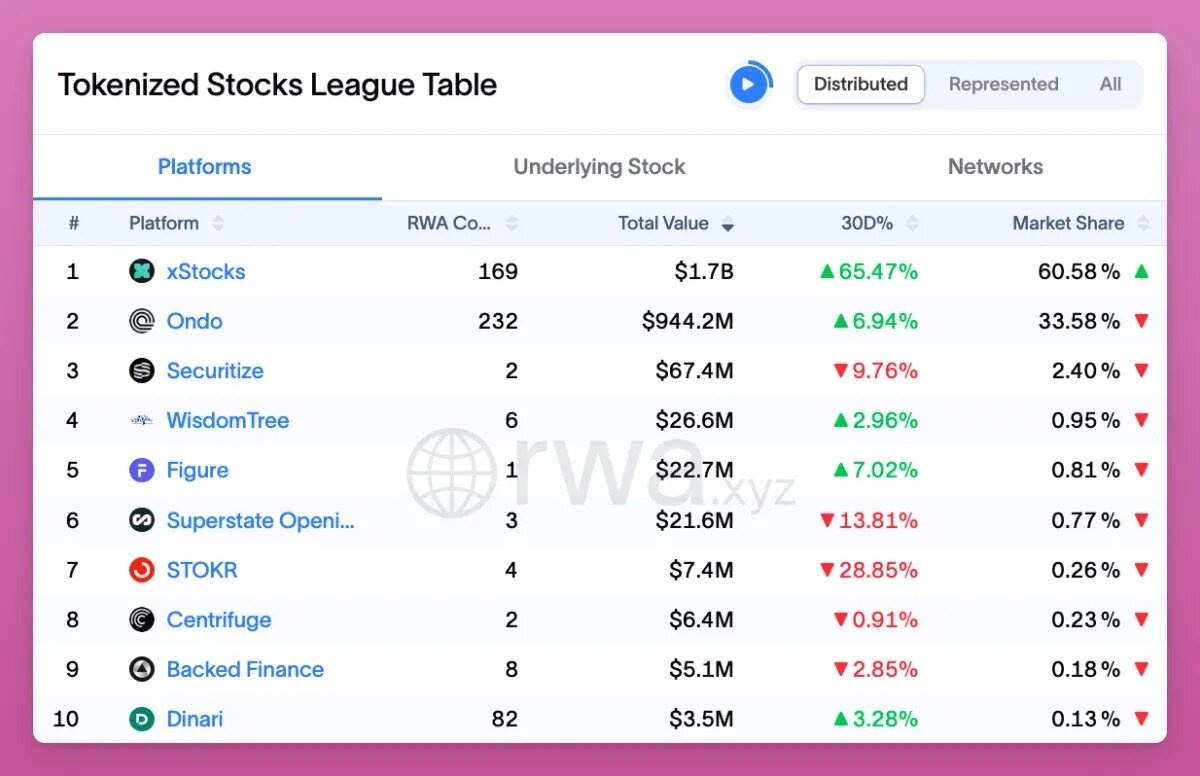

The industry leader xStocks holds 60% of the market share, about $1.7 billion in total. Backed Finance buys real shares, ETFs, and hands them over to the trustees at 1:1 and then casts the currency to track the asset price. The product is deployed in Solana, the Ether (slightly on the second floor of Arbitrum) and the user can trade five days a week at Kraken Exchange or 24 hours a day in the chain, covering about 60 targets. The number of targets is less than Ondo, but the liquidity is better。

The holding of xStock tokens does not amount to holding a bottom-up physical stock, but is a claim against the issuing agency. Once the platform is exposed to risk, the investor is only an unsecured creditor of an encapsulating service provider across the jurisdiction, unlike the Backpack model of holding real equity。

And even more ironically, Kraken bought Backed Finance a few weeks ago and just submitted his IPO application, which was valued at $20 billion. It also casts doubt on whether the platform will issue independent tokens。

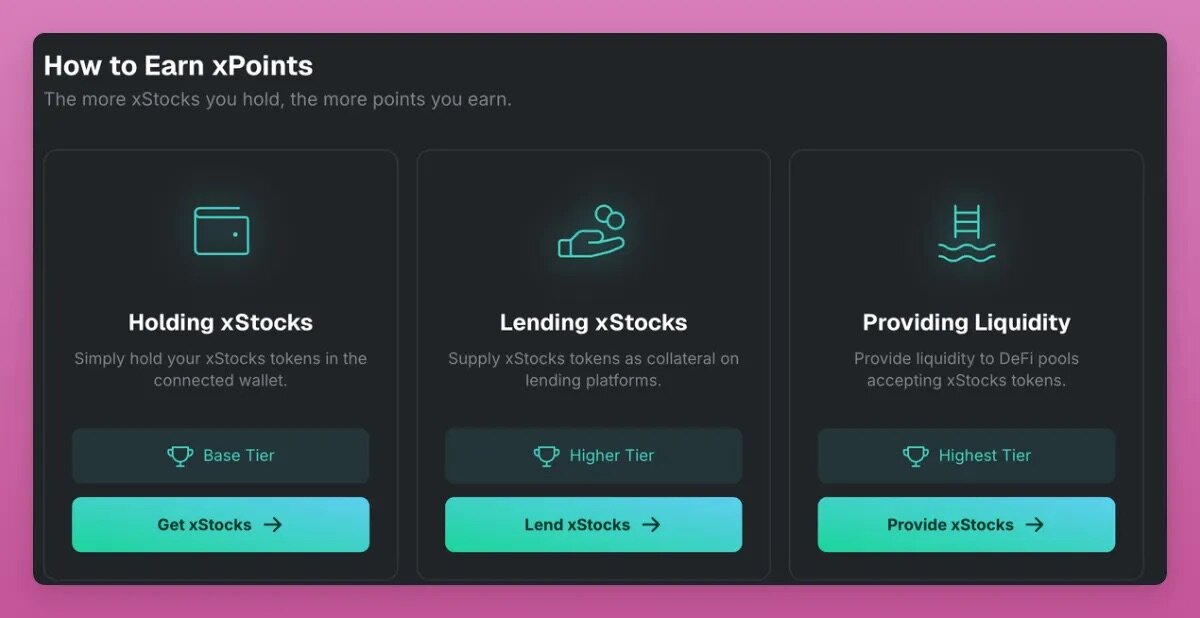

Upon completion of the acquisition, xStocks launched the xPoints crediting exercise in March, which is usually a cushion for the issuing currency, but the platform has not yet confirmed whether it will go online。

xPoints Network of Activists

This is very strange: Kraken itself can sell his own shares through traditional channels, and why issue a single xStocks platform token

A more rational explanation for the roll-out of the crediting scheme is that Kraken is working with NASDAQ in a monetized stock partnership, and that the platform needs transaction volumes and liquidity to support the scale of its operations, thereby boosting Kraken ' s overall performance data。

I don't want to be the pick-up side of the track, but if you want to be part of the extraction, the rules are as follows:

- Provision of liquidity: 7 multiplier points (highest level, support for Raydium, Orca, Byreal)

- Asset lending: 5 multiplier points (Kamino platform)

- Pure possession of token: 1 times base score

- Kraken Centralized Exchange transactions are not counted and chain-only operations accumulate points

The third largest industry is Securitize, and I'm not going to be involved in its mining. The company will be listed through SPAC Shell Cantor Equity Partners, with an overall valuation of approximately $1.25 billion, with a $47 million loan from Belet. The platform has no original currency and no proceeds from mining。

As noted above, there are a number of arbitrage methods in the track: for example, when the financial rate of the contract for perpetuity is negative, you can do it in Hyperliquid (which can also dig mines.xyz credits), Varinational is empty and buy off the spot currency, or on the Ostim platform, which currently has no currency。

If manual storage is too cumbersome to understand the Nado platform: The platform is an order book-based go-to-centre exchange to support cash, bonds, and a single bond account for a lasting contract. The development team built Kraken and launched the INK product. The platform will support spot-and-renewal contracts for monetized stocks and will achieve a delta-neutral strategy. It will be an opportunity for low-profile and deserving mining。

However, it is important to remain vigilant: the first-level market token platform, Ventuals, has just been shut down and users are informed that all platforms have zero value. Participation in the drop-in of coins now requires more energy, and the uncertainty of returns increases significantly。

The story is far from over

The term "encrypted" now has a very wide range of coverage, including sustainable contracts, NFTs, prognostic markets, Meme coins, etc.; the RWA plate also continues to expand in volume, and the subdivision of the tracks deserves to be broken down in depth。

Stabilized currencies, IMF, credit, private equity and monetized shares are subdivided into different types of risk and gain。

The unique advantage of monetized equities lies in the efficiency of asset turnover: equity with its own price fluctuations can generate arbitrage and trading opportunities where passive real world assets do not exist。

I believe that this will bring about a recovery in the main trading chain, which Solana has benefited in particular (I see the ETA as a storage chain for high-value assets, more suitable for passive investment)。

In the past, Solana’s ecology was heavily dependent on Meme coins, and the new narrative of denominated equity "all things can be traded along the chain" might have led to a stronger public chain. For example, in the future, the amount of currencyized equity transactions will or will dominate the chain of solana: transfer fees are low, confirmation speeds are fast, and users experience better than the traditional chain。

Millions of ordinary bulkers may in the future hold, trade, monetize shares at the mobile end, rather than simply deposit stable coins, which would raise ecological revenues in the mainstream chain and thus increase the valuation of public chain coins。

On the whole, the central idea for real wealth growth through the monetization of stock tracks is to bet on the widespread monetization of assets in the chain: which distributors and platforms will lead the course in the next one, three and five years? Which platforms will issue tokens and open airdrops? In fact, the investment mark is right in front of you: you can put on the UNI, the BP, the ONDO, or wait for Kraken to be listed。